In today’s post, I discuss how real estate can accelerate your wealth via exponential growth, courtesy of compounded returns that can beat index funds.

This post may contain affiliate links.

The human experience involves risk

A large part of learning to be a functional human being is learning to assess risk.

Back in the era of cavemen, many of these risks were survival related. For example:

- Is that animal going to try to eat me?

- Is this berry going to poison me?

- Is this cave inhabited by a bear?

Nowadays, if you’re reading this email, you’re lucky enough to be in a position where you don’t have to worry about most mortal threats. You live in a first world country and have the privilege to worry about things like financial risks or risks to your professional reputation.

I think about financial risk a lot. It’s just the way I’m wired and is likely related to some financial trauma in my childhood. Since I like writing, I get to share these thoughts with all of you.

Investing is all about a balance between risk and reward. Again, it’s important to realize that if you’re in a position to even consider these things, you’re lucky. However, just because you’re lucky doesn’t mean that you’re guaranteed financial success.

What is financial success?

For me, I would define financial success as financial freedom, specifically moFIRE. But there are other options. It’s not easy to get to financial freedom, or everyone would already have done it. I would say that it’s almost impossible to get there without investment, absent a few specific instances like a large inheritance or significant business success.

For mere mortals, it will take investing your capital over a number of years, usually decades.

But what I’ve learned over my own financial journey is that it really matters how you invest your money.

If you’re aiming for true wealth growth, you need the power of compounding returns to really have your wealth grow exponentially.

Stocks vs real estate

I’ve transitioned to a real estate focused method of investment over the last half decade.

Part of my reasoning was because I decided that I could achieve better returns in real estate investing than stocks, especially with the various ways that real estate makes you money.

Read more: The 5 ways rental real estate makes you money

This was a calculated risk, because over time, simply investing in stocks is a great way to get to financial freedom. I still invest in stocks via things like retirement plans and 529 educational savings accounts for my kids.

But stocks create gains via only three methods:

- The increased value of the company’s stock

- Preferential capital gains tax rates

- Dividends

While you can get wild gains from investing in individual stocks (ie: the Reddit IPO), I am a firm believer that individual stock picking is no more than gambling for your average investor.

And absent investing in individual stocks, we’re left with index funds or mutual funds. Index funds are comprised of all (or a representative sample) of the stock index it tracks. Good examples of index funds are the Vanguard Total Stock Market Index (VTSAX or VTI) or the Vanguard 500 (VFIAX or VOO). This type of stock investing is very easy, but at best, it’s likely to give you an average return of around 10%.

As a reader pointed out, individual mutual funds can deliver higher returns than the 10% average return of the stock market overall, though consistently selecting the winners is likely trickier than it sounds.

In regards to tax protection, the gains from stocks held longer than 1 year are taxed at a lower capital gains rate (max 20%). Dividends from stocks are typically taxed either at a max of 20% or as ordinary income, depending on if the dividends are “qualified” or “non-qualified.” While better than ordinary income tax rates, this is still inferior to the extreme tax nullification you can get via depreciation in real estate.

In real estate, you can get much higher returns than 10%. There is probably higher risk in real estate investing versus index funds, but this is where we get to decide if we want to take that risk or not.

In my own investing, I’ve decided the risks are worth the gains, and have seen a commensurate increase in my net worth.

Read more: The BRRRR method: how we got a 62% return on our first duplex

Real Estate Syndications vs Stocks

REITs are the stock market version of real estate investing, but their returns are fairly similar to the overall stock market. Real estate syndications, on the other hand, allow sophisticated or accredited investors to invest in larger real estate projects than they could on their own. It also unlocks investments that promise higher gains than index funds.

As I’ve become an investor in syndications myself and now the founder of a real estate investment company, I’ve learned that there’s somewhat of an industry standard for real estate syndication returns.

Read more: The Official Reveal | Cereus Real Estate

Generally, you’re going to want to offer around a 15% compounded return to get the interest of the sophisticated and accredited investors that are allowed to invest in this type of asset.

You might think to yourself that going from a 10% compounded return from index funds to 15% returns doesn’t really make a difference in terms of the long term returns, but you’d be very wrong.

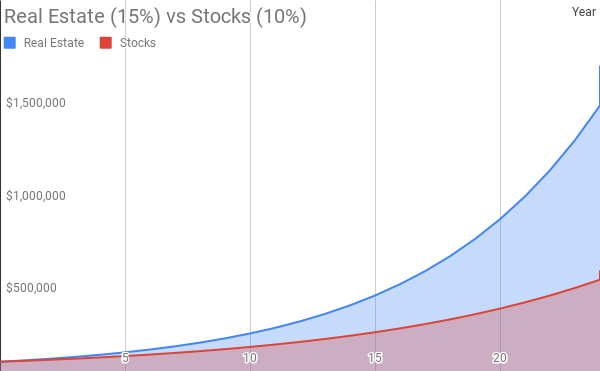

Here’s a chart that shows the destiny of a single $50,000 investment over a 25 year timeline.

At the end of the 25 year timeline, with no further investment of capital, here are the totals:

- Stocks (10% compounding): $541,735

- Real Estate (15% compounding): $1,645,948

Since the life of a real estate syndication deal is usually around 5 years, this would assume that you roll the capital every 5 years into a new real estate syndication. And yes, I would readily admit that your average real estate syndication likely has more risk than simply investing in the Vanguard 500.

However, when I see these curves, it’s not hard for me to decide that it’s worth some risk to end up in the blue curve, rather than the red curve.

The fact is that we only get a certain amount of time on this earth. Therefore, we have to efficiently invest our capital at the highest return possible so we can get to the exponential part of the return curve as soon as possible.

It’s a bit subjective to decide where in these curves you’re really noticing an exponential return rate. And technically, both curves are exponential throughout their curves. They’re actually defined by this formula: A=P×(1+r)t

So instead, let’s ask this question: how long does it take until the investment starts spitting out an annual return greater than the initial investment?

In the example above, how many years does it take for the investment itself to return at least $50,000 per year (which was the value of the initial investment)?

At a 15% compounded return with your typical real estate syndication, you’ll see this at years 14-15, when the value goes from $353,785 to $406,853.

At a 10% compounded return like from your average index fund, it takes considerably longer. It isn’t until years 24-25 when you see a gain greater than the initial $50,000 investment, when the value goes from $492,487 to $541,735.

Therefore, between these two scenarios, you can start seeing major gains 10 years faster with the 15% compounded returns vs the 10% returns.

Conclusion

So I’ve written a lot of words and crunched a lot of numbers for a fairly simple conclusion: It’s better to invest in things with higher returns. My main argument here is that you’ll grow your wealth much faster via real estate syndications, and will start to notice an acceleration in your returns 10 years faster, than sticking with index funds.

Given the national housing crisis, I don’t see the need for housing going down in the near future. And given the relatively high interest rates we’re still seeing today, it’s even harder for people to justify buying a house over just renting an apartment.

Virtually all physicians are accredited investors and now with Cereus Real Estate, you can invest in syndications too! These are exactly the type of deals I’m finding for our investors, personally vetted as much as is humanly possible to try to reduce downside risk. It’s important to know that any investment has the risk to lose money, of course.

I’m trying to get to financial freedom as soon as possible, and I want to bring along as many of my readers as possible!

Why? Because I believe our medical community will be happier, healthier, and more resilient with more financial empowerment. Goodness knows we need more of this, with all of the challenges we have in US healthcare today.

Read more:

- Physicians, No One is Coming to Save Us

- Will Healthcare Survive The Great Resignation?

- The Epidemic of Physician Burnout

I’ve seen the powerful effect of financial empowerment it in my own life, and I want to see it in yours.

– The Darwinian Doctor

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

Your statement that “stocks create gains via only two methods:

The increased value of the company’s stock

Preferential capital gains tax rates” ignores stock dividends, which are a third method by which stocks create gains.

You also say, “And absent investing in individual stocks, we’re left with index funds,” but there are lots of choices of good mutual funds that do not mimic an index. The T. Rowe Price Communications & Tech fund has averaged 14.33% since its inception in 1993.

Good points all around, thank you — I’ll edit my article to reflect this.