Today I give you the real-world performance of my kids’ stock investments via their 529 savings accounts and taxable brokerage account.

This post may contain affiliate links.

Introduction

When I was young, my only investments were a few hundred dollars of savings bonds that my parents bought for me for a birthday when I was young. As my family went through our financial ups and downs, I never really worried about investments. I had no idea that kids could own investments. I thought that investments were something that only rich people had.

Now as a urologic surgeon married to a high earning spouse, we have the luxury of doing things differently for our own children.

By the time I graduated residency training, my student debt from medical school had ballooned to $300,000, but I wasn’t truly worried. I knew that I was headed towards a doctor salary and all of the financial privilege that came with that.

Now about 8 years later, I’m thankfully past the point where I’m really worried about my own financial well being. I still have the luxury of my earning power as a physician, plus multiple streams of passive income via stocks and real estate investments. Aside from my career in medicine, I have a whole new career spreading the message of financial freedom via The Darwinian Doctor and providing passive real estate investment opportunities via Cereus Real Estate. My wife and I are truly blessed.

Read more: The Darwinian Doctor’s Net Worth and Asset Allocation | Early 2022

So now, I can devote some time to ensuring that my children start their life on much firmer financial footing that I did. Below, I’m going to share a couple of things that my wife and I are doing to support that goal. Specifically, I’m going to talk about the performance of my children’s 529 college savings accounts and their stock portfolio.

529 Accounts

My wife and I started 529 accounts for our children from an early age. My older son was born when I was in residency. My wife worked, but we still didn’t have as much money to throw around as we do now. So we began his 529 account around his first birthday. We started my younger son’s 529 account from the same month of his birth.

Since then, we’ve invested $1000 in each of their accounts every month. Although my wife and I suspended our retirement contributions temporarily during our transition from Los Angeles to Memphis, we’ve never stopped investing into their 529 accounts.

We put 100% of the 529 accounts into the Vanguard Total Stock Market Index (VTSAX).

(For those of you who might not know, 529 savings accounts are tax-advantaged investment plans in the U.S. You invest post-tax dollars into these accounts. They grow tax free and come out tax free if you spend them on qualified educational expenses. Parents or relatives typically open them for kids to help pay for college.)

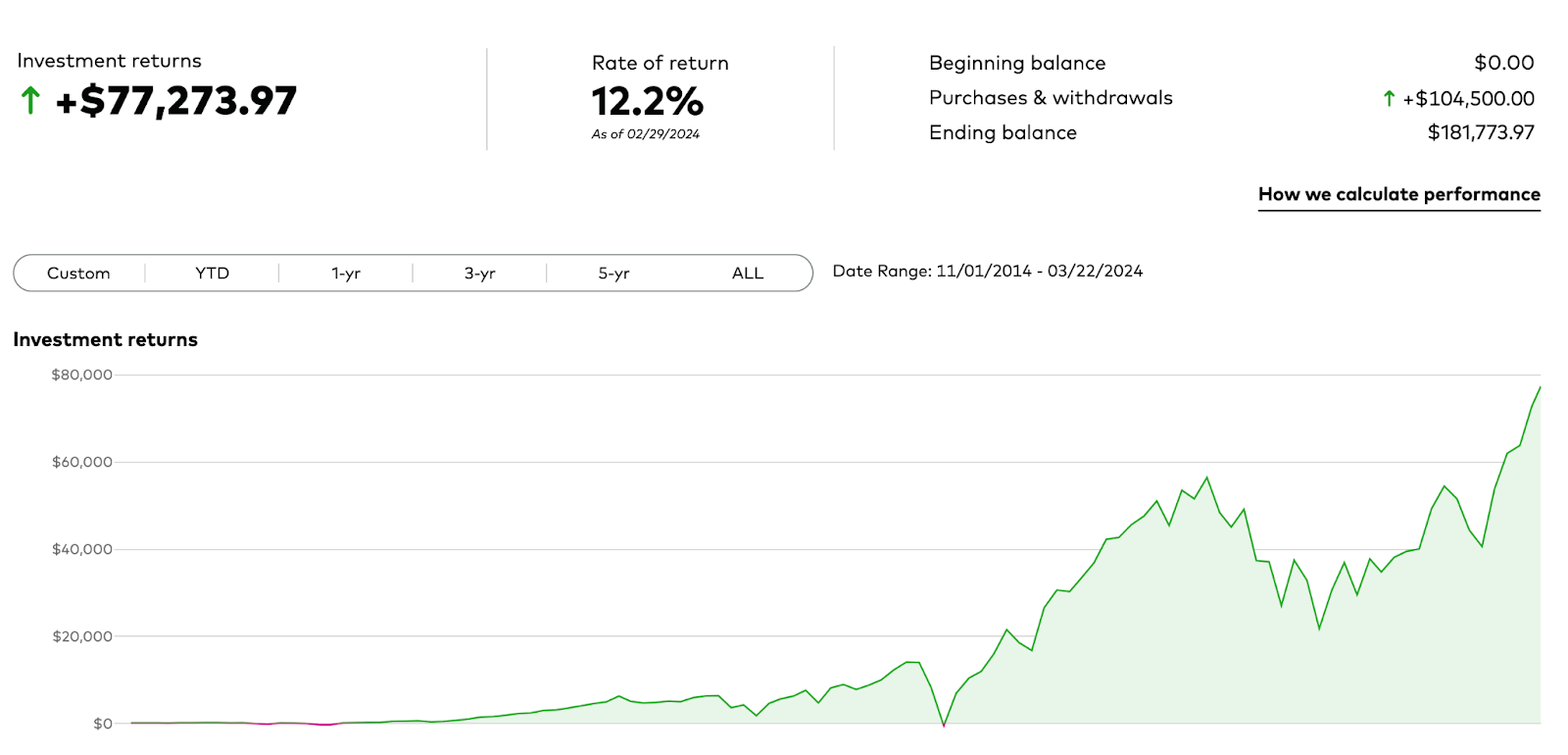

529 performance of my 9 year old’s account

- Money invested: $104,500

- Current value of account: $181,774

- Investment returns: $77,274

- Rate of return: 12.2%

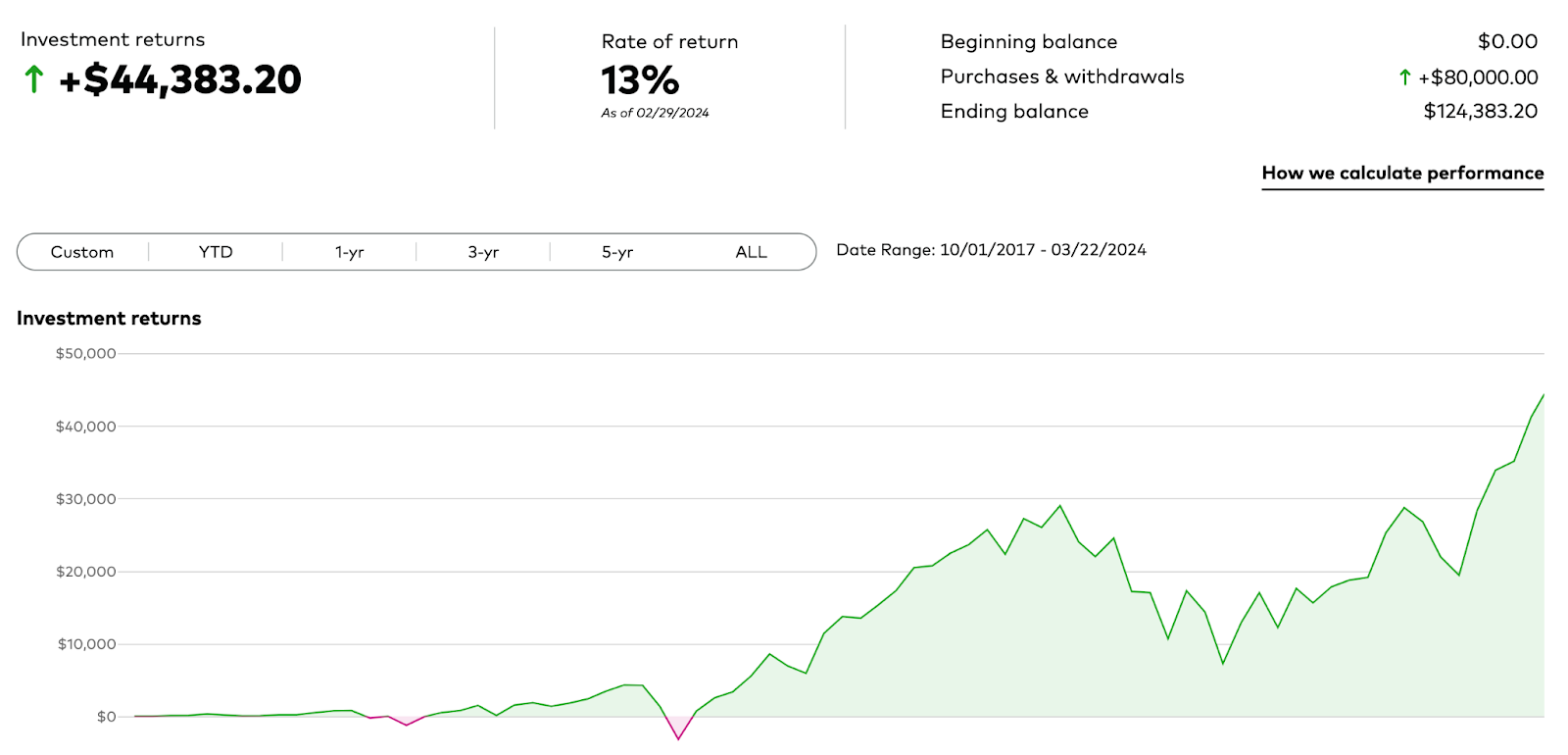

529 performance of my 6 year old’s account

- Money invested: $80,000

- Current value of account: $124,383

- Investment returns: $44,383

- Rate of return: 13%

Overall, the returns on their 529 accounts are a case study of the power of index fund investing in the American stock market. Despite the volatility brought by the Covid pandemic, their accounts have done quite well overall. The historical average of the US stock market is around 10%, so it’s always nice to beat the average.

Taxable brokerage account

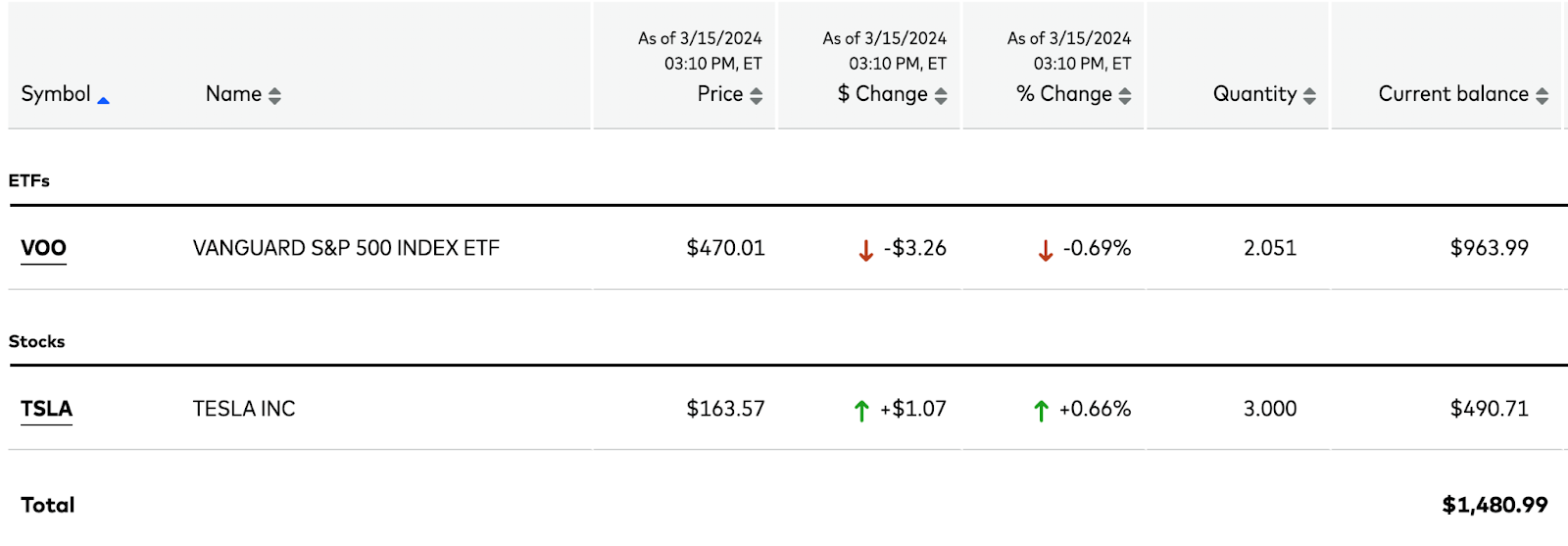

For my older son’s eighth birthday present in 2022, I also started a custodial Vanguard account for him. This is a taxable account, but it’ll allow us to invest money on his behalf. To help teach him about the difference between individual stocks and index funds, I purchased him 1 share of Tesla and 2 shares of the Vanguard S&P 500 index ETF.

- TSLA: $916

- VOO: $759

- Total investment: $1675

Here’s how both investments have done over the last year and a half:

- Vanguard 500 ETF (VOO) has increased by about 25% since August of 2024.

- Tesla (TSLA) has decreased by about 45% since August of 2024.

Therefore, the total value of my son’s custodial account has decreased from $1675 to $1481 over the last year and a half. (Tesla stock did a 3-1 split on August 25, 2022, shortly after I purchased the one share.)

My son and I are both big fans of Tesla as a company, and I’ve invested into their stock in the past. But liking a company and investing into their stock are two different things.

I sat down with my son recently to review this information with him. He was horrified that the value had gone down over the last year and a half. We had a nice discussion about the risk of individual stocks and the decreased risk of index funds. I think he’ll remember our chat for many years to come.

Conclusion

To sum it up, my kids have significant stock market investments in their 529 plans and investment accounts. They are already on firm financial footing compared to where I was at their age. Since we’ve been saving $1000 a month on their behalf, they have hundreds of thousands of dollars saved that will go towards their college education. If their college education is free for some reason, they can spend the money on graduate school or even non-qualified expenses like starting a business. If they do the latter option, they’ll get charged a 10% penalty and will be taxed on the investment earnings of the portion they withdraw. But the basic fact is the money is there for them, invested for their futures.

As you read above, we are also using a regular taxable brokerage account to teach them about the volatility of individual stocks vs index funds. Over time, we hope to accelerate investment into those accounts even more. I hope they will one day use that money to purchase a house or start a business.

When I look at these figures, it’s easy to become used to seeing these large numbers. But all I have to do is think back to when my mom was worried about buying us groceries to put it all into perspective. When I do that, I’m overcome with gratitude for our financial position.

– The Darwinian Doctor

Do you want to do the same thing for your kids? You can start a 529 savings account for free via a number of methods. I like Vanguard, but there are a million options online. (Not an affiliate link.)

To improve your own financial position, I recommend investing in real estate also for many reasons. You can do that passively via Cereus Real Estate (see below). For some deals, you’ll have to be on our investor list to even see them!

Questions or comments? Let me know below!

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions