Today we discuss two of the higher spending options for FIRE: FatFIRE and MoFIRE. These imply spending of $100k and $200k in retirement.

Introduction

Today we’re going to discuss some of the fattier flavors of financial independence, specifically FatFIRE and MoFIRE. Can you handle the richness?

This is the blog post version of Generation Fire Episode 3, a podcast where we bring the goal of financial independence to all generations. You can catch the full recording below!

Last time, we discussed the history of the FIRE movement, which of course stands for financial independence, retire early. We went into some of the figures who founded the movement like Mr. Money Mustache and Vicki Robin. And then we talked about the Trinity study and the 4% role.

Read more: A Brief History of the FIRE Movement | Generation FIRE Episode 2

Today, I want to continue the conversation by specifically going over two types of financial independence. The first one is FatFIRE and the second one is MoFIRE. FatFIRE implies spending over a hundred thousand dollars annually in retirement, while MoFIRE stands for “morbidly obese” FIRE and implies spending over $200,000 in retirement.

Read more: What is moFIRE (morbidly obese FIRE) and why do I want it?

Do you have the wrong idea about FIRE?

I think it’s important to talk about these flavors of financial independence because a lot of people have the wrong idea about financial independence. Many people think that just because someone is seeking FIRE, they’re a penny pinching miser and also lazy because they’re seeking early retirement.

We discussed at the end of last episode how early retirement is actually completely optional once you’ve attained financial independence. In fact, all of the people that I personally know who have achieved early financial independence have continued to work. The main difference is that they’re in complete control of their day-to-day schedule, and they get to do exactly the kind of work that brings them joy.

In an ideal scenario, work is something that brings both satisfaction and intellectual stimulation, so I can understand why people continue to work after financial independence. It’s part of the reason why I still work despite being in a very fortunate position where I have a mix of income options beyond my surgical income alone.

So the true goal that drives me now is to move as many people as possible towards financial freedom, primarily through the power of real estate investment.

Speaking of real estate, are you interested in passively investing in this asset class? Maybe you should check out Cereus Real Estate! We officially launched in January and we’re actively signing up potential investors for real estate investments. We’re a real estate company founded by physicians, and our goal is to offer high quality real estate investment opportunities to help move you closer to financial freedom. Come and check us out!

Experience the financial benefits of real estate without dealing with the headache!

FatFIRE

As I mentioned above, FatFIRE implies spending at least $100,000 annually in retirement. This is over $8,000 a month, which for most people is sufficient to live a good quality of life in most cities in our country. This amount of money will go even further in retirement when you consider that most people in retirement aim to have most of their debts paid off.

For example, imagine your living costs if you didn’t have student loans, a mortgage, or a car payment. Eight thousand dollars a month would go a long way.

FatFIRE means less limits

People who are aiming for FatFIRE don’t want to be so limited in their spending in retirement. They want to be able to go out to restaurants and have the ability to travel modestly to see friends and family.

The math behind FatFIRE

If you’re interested in a FatFIRE level of retirement, by the 4% rule you need to have at least $2.5 million saved in a mix of stocks and bonds at the time of your retirement.

To review, the 4% rule is from the Trinity Study, which showed that with a mix of stocks and bonds, you can safely withdraw up to 4% of your nest egg without the risk of depleting your funds over a 30 year time period.

Two and a half million dollars is a lot of money, so let’s take a moment to discuss what you’d have to do to save that much money by retirement. Spoiler alert, it’s not as hard as you might think.

How to save $2.5 million

To save $2.5 million, you do need to consistently save money and invest it into the stock market. But as you’ll see below, the more important elements in this equation are arguably time and the magic of compound interest.

If we assume an 8% average annual return in the stock market, which is historically accurate, you only need to put away a fraction of that $2.5 million as long as you have time on your hands.

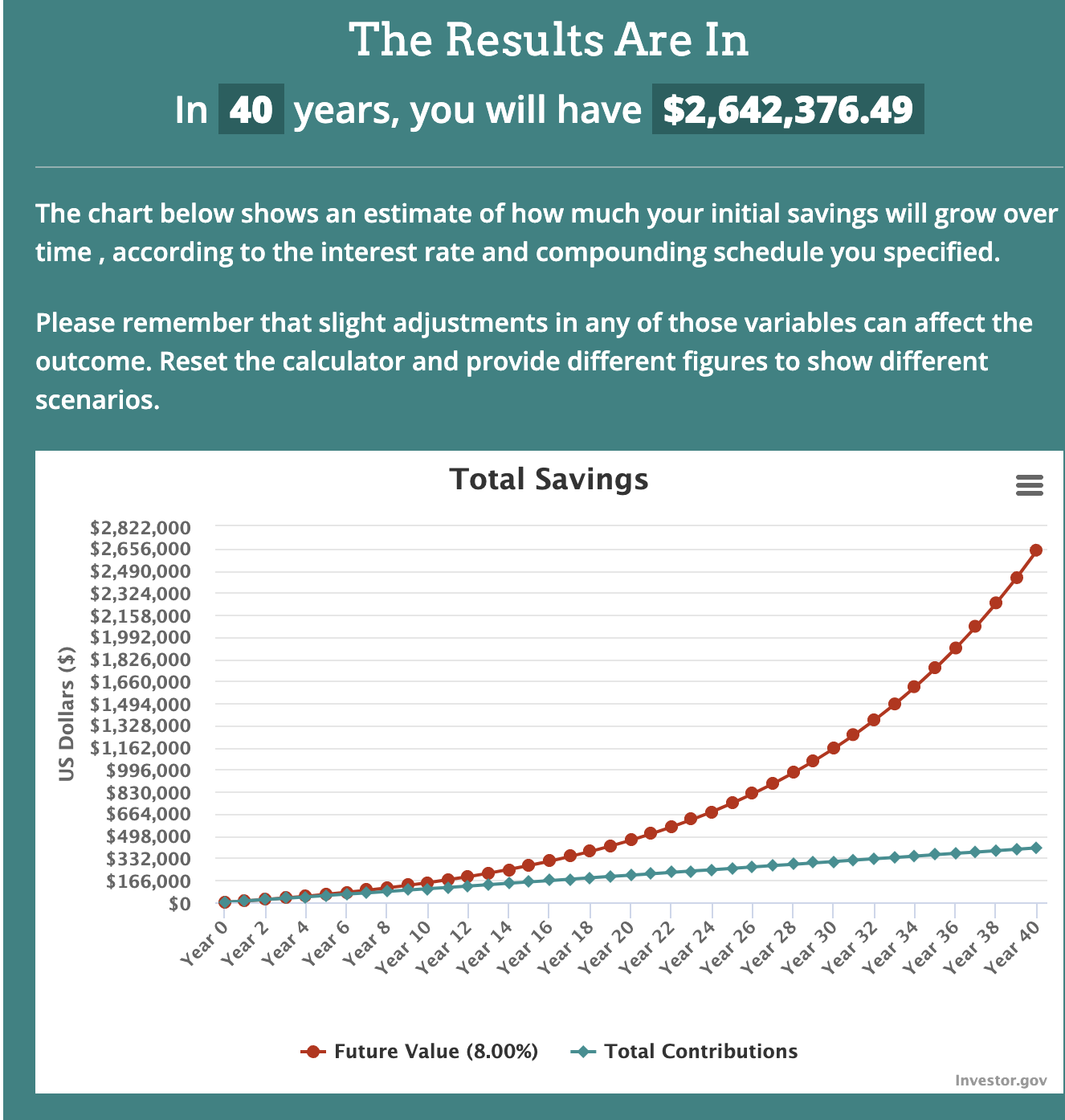

Here’s the surprising math behind saving $2.5 million:

- Start at 25 years of age

- Save $850/month for 40 years

- Invest the money into stocks with an 8% return

That’s it! In this 40 year time period, you’ve only contributed $408,000. However, due to the magic of compound interest, that $408,000 will grow to over $2.6 million over 40 years.

A note about inflation

This is probably a good time to address an important factor in any talk about financial independence, and that’s inflation. Over the last year, everyone has seen the pretty drastic effect that inflation can have on your day-to-day cost of living.

Inflation does seem to be coming under control now, but you can see easily that if you don’t factor in this economic force, your retirement calculations might be totally worthless. So anytime that I look forward to the future, I assume a 4% inflation rate in the cost of living.

This might apply to things like groceries, gas, and things like entertainment. I think you could effectively argue that some categories like healthcare and college tuition should probably have even a higher expected rate of inflation. You’re probably right about that, but let’s leave that nuance for another day. Now, let’s talk about my favorite flavor of financial independence: MoFIRE.

MoFIRE

MoFIRE stands for “Morbidly Obese” FIRE and it implies spending north of $200,000 a year in retirement. That’s around $16,700 a month.

With $200,000 a year, people who’ve achieved MoFIRE can have significantly more options in terms of living, eating and travel. Instead of just traveling in the continental United States, for example, you can easily travel to Europe a couple times a year.

Instead of limiting your restaurant choices, you can also throw in a few Michelin star restaurants to really expand your palate. And if you’re going to be renting a place in retirement, you’ll have a much wider range of options with a MoFIRE level of spending.

I aspire to MoFIRE

For me, I aspire to at least a MoFIRE level of spending in retirement. My longtime readers might recall this post, where I outlined our annual spending. This was about six years ago when I first started on this journey towards financial freedom. We’ve made a lot of changes in our life, but because of the phenomenon of hedonic adaptation, it would be fairly difficult for my family to move backwards in terms of quality of life.

FIRE is about security

While this might be a personal thing, I like to think about FIRE in the context of the word security. Just because you’ve achieved FatFIRE doesn’t mean that the retirement police are going to make sure that you spend at least $100,000 a year.

The important thing is that you can spend up to that amount if you’d like to do so. Through hard work, saving, and investment, you’ve built up an unassailable nest egg that can sustain you through thick and thin.

So for some people who are generally suspicious of the 4% rule and the concept of financial freedom, setting a large goal like FatFIRE might be the right move.

Again, you don’t need to spend a hundred thousand dollars in retirement just because you’ve achieved FatFIRE, but if you want to, you can safely do so.

Conclusion

So if you thought the financial freedom movement is all about saltine crackers and sardines, now you know that there’s a wide variety of levels out there for you to consider.

Today we discussed FatFIRE and MoFIRE, which respectively entail the ability to spend at least $100,000 and $200,000 a year in retirement.

I personally know a lot of physicians who are working towards at least a FatFIRE level of financial freedom. I’m working towards MoFIRE, which is also known as morbidly obese FIRE.

Again, you can check out the corresponding YouTube video podcast on this topic. The next episode I’ve got planned will address some of the leaner flavors of FIRE, such as LeanFIRE, BaristaFIREand CoastFIRE.

See you then!

– The Darwinian Doctor

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

I’m going for My 600 lb life level of FIRE – $10M in the bag!

With all do respect, this article is pretty ridiculous. First, all these different types of FIRE are just crazy. Just made up so someone can have an article to write about to get clicks. I mean, to me having fat and mo fire is just excessive.

Second, this arbitrary assigning of 100k and 200k is crazy too. I can guarantee I wouldn’t feel anywhere close to fatfire or mofire with those levels of spending. Heck, 100k could be both lean fire and mofire just based off where someone lives. Even in lower cost of living areas, do you think 200k will make you feel good if you like to travel? If I am mofire, a 4k business flight is nothing to me. You aren’t traveling much with a significant other at that level of spending.

So you’re saying fatFIRE for you is more about an ability to do X in retirement? How would you define your target level of financial freedom?