Today we discuss the fastest way to improve your credit score using the credit utilization factor!

Part of the “Road to rental real estate” series: This is part of a new series that will document my attempts to diversify my investments using rental real estate.

On the way to moFIRE!

As part of my path to moFIRE, I am planning to repurpose some of my investment capital into cash flowing rental real estate. While accumulation of wealth in both retirement and taxable accounts is a sure and steady path to financial independence (FI), cash flow producing investments have a unique ability to significantly drop the amount of cash needed to get to your “FI number.”

Turnkey real estate

One option for beginner real estate investors to get started with real estate investment is called “turnkey” real estate. “Turnkey” is a catchy descriptor developed by the real estate industry to describe a rental property that has been purchased, rehabbed, and tenanted by a company, which then sells the finished product to an investor. Often times, the same company will then provide property management services to the investor.

The goal of the turnkey provider is to decrease the major barriers to the purchase of rental real estate, for a price. With varying degrees of transparency, the turnkey provider will mark up the properties, and pocket the difference between the final sales price and their costs to purchase, rehab, and tenant the property. Seasoned real estate investors will often criticise this markup, and rightly realize that with enough time and effort, they could likely produce a similar product with significantly lower cost (and higher returns).

But for the busy professional, the expertise and services provided by the real estate professionals might provide enough benefit to make the markup palatable.

For now, I’m in this latter camp. While I considered “doing the work myself,” and assembling a team to help purchase, rehab, and rent out property, I’ve shied away from actually pulling the trigger. I have some friends who are doing this with varied degrees of success, but the initial stages are incredibly time consuming. The later stages of property management can also be time consuming, even with the help of professional property management.

I figure that I might as well ease into rental property ownership using the turnkey model, and if I like it, I can use the experience to consider going more “do-it-yourself” in the future if all goes well.

Update: I’ve taken the plunge into active real estate investing and am growing a rental empire! Check out how my real estate portfolio is doing here.

Walking in Memphis

So I recently made a trip to Memphis, Tennessee to peek under the hood of a well respected provider of turnkey rental homes. I liked what I saw, and I should be ready to purchase my first rental home within a couple of months. If all goes well, I’ll write a detailed post about the provider.

Checking my credit score

In anticipation of financing the property, I did a soft credit inquiry with one of my credit card providers, Chase Bank. A “soft” credit pull is different from a “hard” credit pull in that the soft pull doesn’t negatively impact your credit score. The caveat is that the soft credit pull might not generate the exact score that the bank sees when you apply for a mortgage.

Popular services such as Credit Karma and Credit Sesame use VantageScore credit scores, which is a formula that uses information from one or more of the three major credit reporting bureaus (Equifax, Experian, and TransUnion) to estimate credit worthiness. This differs from the FICO score, which is a score generated using the same information, but from the Fair Isaac Corporation. The FICO score is the one relied on by most of the major creditors, like banks and credit card companies.

It’s actually free for you to get your own credit score once a year from the three major credit reporting bureaus. This has been the case in the USA since 2003, when the Fair and Accurate Credit Transactions Act was passed as an amendment to the Fair Credit Reporting Act. You can do this by going to annualcreditreport.com. (Beware of imposter websites looking to rip off your data!)

It’s not free for third parties to access your data on your behalf. So the free services offering credit monitoring will often pay for their costs via advertising or some other angle. That doesn’t make the services any less useful, but it’s important to be aware of this fact.

For this post, I used a service linked to my Chase credit card called Credit Journey. This service estimates your credit score via a VantageScore generated from TransUnion. What I like about this service is that it also offers a nifty calculator function that lets you model actionable changes and recalculate your score based on those changes.

My credit score is… OK

When I checked my score recently, I was surprised to that my score was estimated at 735, well under the magical score of 760! When it comes to mortgages, those with scores above 760 qualify for the best mortgage rates. I’ve read various sources stating this magical number to be 740, but the originator of the FICO score itself, the Fair Isaac Corporation, states the best rate score to be 760.

The mortgage rate matters because over the course of a loan, just a slight difference in interest rate can make a huge difference in how much interest you will pay.

Mortgage rates based on FICO score

($200,000 mortgage amortized over 30 years)

| FICO Score | Mortgage Rate* | Interest Paid |

| 760+ | 3.798 % | $135,407 |

| 700-760 | 4.02 % | $144,570 |

| 680-699 | 4.197 % | $151,966 |

| 660-679 | 4.411 % | $161,016 |

| 640-659 | 4.841 % | $179,545 |

| 620-639 | 5.387 % | $203,718 |

*Rates as of March 2019

Source: Fair Isaac Corporation

As you can see, for a typical $200k mortgage, those with the best credit scores will pay $68,311 less in interest over the life of the loan than those with the lowest scores!

I was surprised that my estimated FICO score wasn’t above 760. After all, I make a high income, faithfully make my mortgage and student loan payments every month, and pay off all my credit cards in full each month. There are no defaults or bankruptcies on my books either.

I did some research to figure out why my credit score wasn’t in the best category. What I found really surprised me.

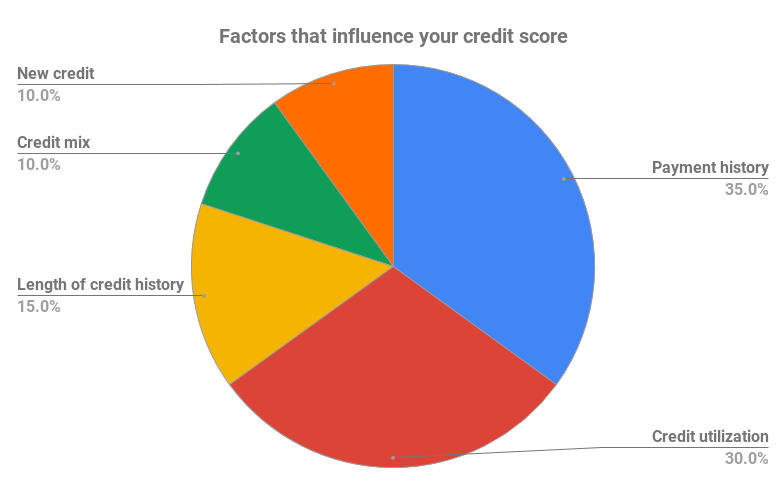

Factors that influence your credit score

While there are minor differences depending on which credit bureau you are dealing with, it’s generally correct that the bureaus use something close to this breakdown:

Payment history: 35%

Basically, this category asks the question, “Does this borrower make all her payments on time?” This applies for “revolving credit” like credit cards, and also installment credit, like student loan and mortgage payments. Bankruptcies and loan defaults are quite damaging, and will stay on your report for 7-10 years.

This makes sense. Past behavior is a strong predictor of future behavior, and thus this category is the most important of all in determining how risky it is to extend credit to you.

Credit utilization: 30%

This category explores how much of your available credit you are using. Credit companies generally have found that if you are consistently maxing out your credit cards each month, you are at a higher risk of credit default.

Most sources recommend keeping the balance on your cards at less than 30% of the available credit. Lower than 30% is even better.

Length of credit history: 15%

I found this category quite annoying. It turns out that for the purposes of your credit score, the bureaus are specifically looking at the length of time you’ve carried so called “revolving credit,” which is short for credit cards. The longer the better.

All of those years of on-time mortgage and student loan payments don’t seem to come into play for this category.

It does seem that the system gives you some points for time spent as an authorized user on your spouse’s or parents’ credit card, but it’s unclear how much. Joint accounts would logically help more, because both users of a joint account are financially responsible for any defaults. But I couldn’t find hard data on exactly how much the formulas take this all into account.

Credit mix: 10%

This category takes into account the different types of credit on your history. A varied mix of credit cards and installment credit like loan payments is better than someone who has never utilized a credit card before.

New credit: 10%

This category reflects the number of hard credit checks (or pulls) in your recent history. All hard credit pulls are visible on your account for 24 months, but only negatively affect your score for 12 months. Opening a lot of credit lines in a short period of time is viewed as risky behavior.

Each inquiry can drop your score by 5-10 points, but generally, rate shopping is treated as just one inquiry. For example, if you apply for a car loan with four different credit unions within a 14 day period, this will be just treated as one inquiry.

This also may seem like a particularly annoying category, but it has been shown that people with 8 inquiries on their credit report are 6 times as risky than people with no inquiries. (Reference: McCorkell, Peter L. “Comment: Managing Credit Risk Means Getting the Right Mix,” American Banker (March 20, 1996), p. 14.)

So what can be changed in the short term?

When I went through all the categories, the only thing that can be changed in the short term is length of credit history and credit utilization.

To increase the length of your credit history without the use of a time machine, become an authorized or joint user on a spouse or parents’ credit card. If their credit history is longer than yours, some of their credit history can be counted as your own. This should help a little, but it doesn’t seem to have the ability to greatly increase your score.

Credit utilization alone comprises 30% of your credit score. It’s measured on a frequent basis, making it something that can change quickly. To quickly gain points in this category, keep the balances on all your cards as low as possible. Definitely keep it below 30% of your credit limit.

This can be tough if your cards have low limits, so one strategy is to ask for higher limits on your credit cards. This strategy can be counterproductive, however, since each time this is done, there is generally another hard check on your credit score that will drop your score 5-10 points.

If you find yourself struggling with keeping your balances low, you could of course just spend less on your credit cards. But you knew that already.

Credit utilization is usually reported to the credit bureaus on a monthly basis. But this varies from one credit card company to the next. So one strategy, is to just pay off your credit cards in full on a weekly basis.

The effect of keeping credit card balances low

When I utilized the Chase Credit Journey tool, I found some encouraging results.

When I plug in my information, my estimated FICO score is 735.

But if I lower the balance on all my cards by $1000, my score shoots up by 22 points to 757!. This is close to the best mortgage rate zone (760+).

Conclusion

So to rehab my credit score before I need to apply for a new mortgage for the rental property, I am going to do a few things:

- Fully pay off all my credit cards on a weekly basis to keep my credit utilization low

- Stop authorizing hard credit pulls for new credit until I start mortgage shopping

- Call all my credit card providers and ask if they will increase my limits without a hard credit check.

I’ll report back soon to see if my efforts have paid off.

-TDD

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions