In today’s post, I’ll explain how to become rich. It’s not rocket science, but it might take a little legwork. Interested? Read on.

This post may contain affiliate links.

I was surprised when I recently realized that my blog doesn’t have a post about the basics of personal finance. While I bet most of my readers already know this, you know what they say about assumptions…

So below, here’s a very basic outline about how to set yourself on the path to financial stability and abundance. Let me be clear — if you follow these principles, you’ll end up rich (with time). As a disclaimer, each of these topics deserves (and eventually will have) more written about them on this blog. But for now, please use this as a basis for our future discussions.

Here are 6 Steps to Save, Invest, and Become Rich:

- Map out your income and expenses

- Grow the gap

- Save an emergency fund

- Pay off high interest debt

- Invest regularly

- Wait

There are a million ways to make this quite complicated, but really, these are the basics. If you do these 6 things, you’ll eventually become rich.

“Rich” vs FIRE

“Rich” is a relative term. I used the term mainly to add a little click-bait element to the title. But in reality, my default assumption is that you’re not just aiming to become rich. I think you should aim higher.

Many high income professionals are “rich” in the eyes of society by virtue of their income alone. But if you don’t hold onto a portion of that income and invest it, you’re a slave to your job to maintain your lifestyle. That doesn’t seem very “rich” to me.

That’s why I aim for financial independence (FIRE), and I think you should too. FIRE is short for financial independence, retire early.

FIRE is a state of being where your passive income pays for all of your expenses, giving you the power to retire early (if you so desire). Specifically, I’m working on achieving moFIRE within 10 years or less. Morbidly obese FIRE (moFIRE) allows for annual spending of > $200,000.

I don’t want to preach on this too much here, but read these posts for more on this topic.

- What is moFIRE (morbidly obese FIRE) and why do I want it?

- Physicians are trapped by golden handcuffs

- Why the rich don’t feel rich

Proof of concept

You might be thinking to yourself that it’s impossible with your income (or spending habits) to become “rich” or achieve FIRE. I don’t agree. Below, I’ll show you some simple data to show how straightforward it can be to become rich.

Here’s how to get to $1 million over a 30 year time horizon:

- Invest $736 every month at an 8% return.

- Reach $1,000,517 after 30 years.

- That’s it.

Although $1 million dollars isn’t what it used to be, most would still agree that this is a lot of money. To figure out how to get there, you just need to use a compound interest calculator.

Isn’t it surprising how little money it takes to get to a million dollars with the help of compounding?

That’s all well and good, you might be saying. But how do you actually do this? Well I’m glad you asked.

1. Map out your income and expenses

To know if you have money to invest, you need to have an understanding of your income and expenses.

So first, take a look at your paychecks for the past few months to find out your income.

Income

Find the detailed view of your paycheck, so you can see if you’re already contributing to savings via something like a 401k. You can also look to make sure taxes and benefits are already deducted from your paychecks.

After this sleuthing, you should have a general sense of what you’re making every 2-4 weeks. If your income is variable, you can average it over 6-12 months.

This amount is your income. Put it into a spreadsheet.

Do you have any side gigs that bring in additional income? Log that too.

Expenses

Examining your expenses will be illuminating (or horrifying). Take a look at all your recurring expenses. These are the basic costs of your life. Here is a list to get you started (in no particular order):

- Internet and streaming services

- Utility bills (water, electric, gas)

- Car payments (transportation)

- Rent or mortgage payments

- Property taxes (if applicable)

- Restaurants/entertainment

- Student loan payments

- Credit card payments

- Cell phone service

- Groceries

- Childcare

- Clothing

- Other

Obviously, some of these will apply to your life, and some will not. But for most of us, this list of expenses will comprise the majority of the expenses that consume your income every month.

In modern society, you need to pay for these for your life to function normally.

The “other” category could be pretty variable. For us, this represents one-off expenditures, like Amazon purchases and electronics.

If some of these costs seem larger than you expected, don’t be surprised. It’s sometimes hard to keep track of expenses until you write everything down. Unless you sit down and do this basic step, you really have no idea where all your money is going.

I was shocked when we calculated our full monthly expenditures. Read about it here: The Darwinian Doctor’s 13 Monthly Expenditures (with real numbers)

Add together all your monthly expenses and subtract this from your monthly income. The leftover money is your “gap.” This is going to be the fuel for your savings, investment, and future riches.

This is supposed to be a positive number. If it’s not, or if it’s a very small number, fear not. Move onto the next step.

2. Grow the gap

Now this is the fun part. In the past step, we got a rough estimate of your monthly income versus your expenditures. This is the basis of your entire financial plan. The leftover money is what is commonly called “the gap.” If there’s no gap, or it’s too small, you’ll never stop working. You’ll have to keep working for the rest of your life to pay for your recurring costs.

If you do have extra money each month, fantastic. But you want this gap to be sizeable if you’re ever going to become rich or hit FIRE.

So you have to grow the gap. There are two ways to do this:

- Decrease your expenditures

- Increase your income

Let’s take them one by one.

Decrease your expenditures

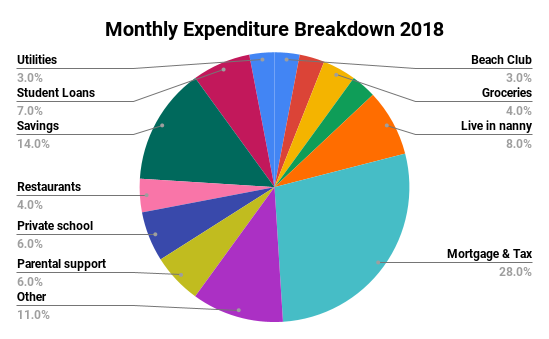

Take a look at your expenditures from step one. Think about how much of your income each one is eating up. Is that OK with you? If you want to get fancy, you can chart this out. This is mine from 2018:

Think critically about each expenditure and come up with a plan to decrease the cost.

There are many different ways to decrease your spending. Here are a few ideas to consider:

- Stop paying for cable and sign up for streaming

- Be mindful of your water and electricity use

- Refinance your student debt

For most people, the biggest savings are going to come from lowering the cost of your housing and transportation.

You can see above that for me, the monthly payment on our house is our biggest single expense. For us, there’s an argument that home ownership has been a good wealth builder, but this isn’t always the case.

When you think about your costs, go ahead and ask yourself: How much do I want to have financial security and get off the hamster wheel?

Then get ready to make some sacrifices. Move to a smaller house. Get rid of the expensive car and get a used car instead.

Easier said than done, right? My wife and I argue politely discuss this topic a lot, and for now we’ve ruled out a big move to a lower cost of living area. I also would go insane without my Tesla’s autopilot and the HOV lane sticker it allows, so I’m stuck with that car payment as well.

Honestly, we’ve focused on the other option more:

Increase your income

No matter your situation, there are always options to make more money. Here are some of the best ways to quickly increase your income:

- Ask for a raise

- Work more hours

- Change to a better paying job

- Start a side hustle a business

The Covid-19 pandemic caused most people to re-evaluate their employment. This makes it a great time to demand more from your employer: more money, more benefits, or more flexibility.

There’s even a controversial trend now where remote workers (secretly) hold two jobs at once!

Although I don’t think anyone has conclusively figured out why there is a nation-wide labor shortage, many employers are desperately seeking workers right now. This makes it a fantastic time to try to improve your employment situation.

My wife and I are already at the higher end of income opportunity, so we’ve focused on the last option for increasing income: starting your own business.

Together we’ve built an empire of rental real estate that we hope will bring us to financial freedom within the next 5-10 years.

But there are a million and one ways to get extra income on the side. Here are 50 ideas to get you started from Entrepreneur.com.

3. Save an emergency fund

When you’ve grown your gap, you should save up an emergency fund to insulate against the damaging effects of random expenses.

The best financial plan isn’t useful if it can be derailed by a flat tire or dental emergency. You need a buffer of cash so you have enough money to pay for life’s little surprises.

So save up a reasonable emergency fund and only use it for emergencies. The amount of the fund varies from person to person.

Dave Ramsey recommends starting with a $1000 emergency fund. Then when you’re more financially stable, expand this to 3-6 months of expenses.

I think this is a great way to start out. Put the emergency fund in a bank account that’s different from the one you use for everyday spending. That way, you won’t accidentally spend it.

As your assets grow and you get access to low interest sources of credit like HELOCs or SBLOCs, you can consider using those instead as your emergency fund. But in the beginning, it’s far safer to have your emergency fund in cold hard cash (in the bank).

4. Pay off high-interest debt

It will be a lot harder to become wealthy and rich if your money is eroded every month by high interest debt. The OG of FIRE blogging, Mr. Money Mustache, often calls high interest debt as a “hair on fire” emergency.

What’s high interest debt? Debt on credit cards and high interest loans are emergencies. Arbitrarily, I feel that anything that’s charging you 3x the average home mortgage rate is an emergency and should be paid down.

At the time of this article, Bankrate reports that the average mortgage rate is 3.25%.

Triple that is 9.75%. If you’ve got debt that is charging you this much or more, please pay it down, or it’ll be very difficult to make any progress towards real wealth.

If you have student loans that are near this high interest rate, please consider refinancing that debt right away.

5. Invest regularly

Once you’ve got the first few steps down, it’s time to move onto investment. This is an incredibly important step. Without investment, inflation will eat away at your savings and your net worth will decrease as soon as you stop saving.

Luckily, investment doesn’t have to be hard.

Investment made easy.

Many people invest in their retirement accounts. This is a great option, and often times your company will have a human resources department to help you do this.

But whether you have access to retirement funds or not, the concept is still the same. For a simple and reliable form of investing, this is all you have to do:

- Open up an account at Vanguard, Fidelity, or Schwab

- Purchase shares of VTSAX (Vanguard Total Stock Market Index)

That’s it. Set up automatic investment that takes place every time you get paid. This way, the money is automatically withdrawn from your checking account without action on your part.

VTSAX is a great index fund option. An index fund is one of many mutual funds where for a small price, you can own a tiny piece of many companies in the US. With one share of VTSAX, you can own a small piece of > 3600 companies.

For more on why you should pick VTSAX, please read my review of the Simple Path to Wealth.

With this single approach, over time you should return about 8-10% on your money. With disciplined investing, this will compound over time and grow to dizzying sums of money.

Advanced investing

If you want to chase higher returns and are willing to take on additional risk, there are again a million and one ways to do this. I’m finding higher returns via real estate investing, but rest assured that this is completely optional. I also invest a small part of my income into individual stocks, but I see this as akin to gambling.

6. Wait

This final step is important enough that I wanted to dedicate a section to it. Investing is a long term method of building wealth because compound growth takes time. Unless you win the lottery or you just happened to invest in Tesla before it blew up last year, you will need time to achieve your financial goals.

If you refer back to the compound interest graph above, things don’t start to get exciting until around year 9 or 10. That’s when your money gets busy, making beautiful money babies of its own every year. It’s around year 10 of regular investment when the money generated by the index funds is greater than your annual contribution itself!

There may be recessions or bear markets, but time heals all wounds, and the market always goes up. Barring the end of civilization or the fall of the United States, all you need to do to become rich is invest and wait.

Conclusion

I hope you enjoyed this post on How to Save, Invest, and Become Rich. Here are the six steps listed again:

- Map out your income and expenses

- Grow the gap

- Save an emergency fund

- Pay off high interest debt

- Invest regularly

- Wait

This plan is a reliable path to financial success. It can take some hard work to “grow the gap,” but the rest of these steps form a simple and reliable path to becoming rich. More importantly, these steps will also eventually buy you financial freedom and perhaps the ability to FIRE.

There’s also endless variety when it comes to investing. You can follow in my footsteps and buy rental properties or keep it simple and invest in a diversified portfolio of stocks and let compound interest do its thing. What you cannot do is stay ignorant of your financial position. When it comes to your financial journey, inactivity is much riskier than the financial risk from investing.

And finally, please keep in mind that the ultimate goal is not to be a rich person or to have lots of money. Money is a tool. I recommend you use it to buy you financial independence to have freedom over your most valuable asset: time.

For me, that’s the goal of all my saving and real estate investments — to create the cash flow necessary for true financial freedom so I can live my best life.

–TDD

What is your method to save and become rich? Comment below and please subscribe to my free weekly newsletter!

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

Posts like how to save and invest needs to be in every high school curriculum so that children can learn how to be successful from a young age. Many of my peers mock me for saving and investing so much and I can’t imagine just what kind of financial health situation they are in.

I agree! It needs to become part of everyone’s normal education to empower the future generations. Your friends won’t be mocking you in 10 or 20 years, that’s for sure.