Today I show you with our real data how focusing on rental cash flow cut 5 years off our original timeline to moFIRE.

This post may contain affiliate links.

It’s been roughly two years since my original “15 year plan to financial independence, moFIRE style.” “MoFIRE” refers to morbidly obese financial independence, retire early, and implies the ability to maintain an annual level of spending in retirement > $200k.

In this plan, I outlined an aggressive, 15 year timeline to financial independence. It had three important elements:

- Hold expenditures steady

- Max out retirement accounts

- Invest increasing amounts into our taxable and 529 accounts

With our plans of aggressive saving and index fund investing, we were originally set to be financially independent with $8.75 million of investments by 2032.

Side note: I admit that it’s a blessing that the Dr-ess and I are in a position to not only cover our expenditures and also save money. We worked hard to get here, but we had certainly had advantages along the way.

The transition to real estate

It was about a year after I published this 15 year plan when I had my realization that rental real estate has incredible benefits as an investment vehicle, specifically:

I made an abrupt transition to real estate investing, and the it’s been full steam ahead. But this all begs the question: Is real estate investing actually speeding up our journey to moFIRE?

An error in my calculations

First of all, I want to revisit my “target.” In my original plan to achieve moFIRE, I saw that $254,000 of our annual expenditures were recurring costs that would continue even if we retired immediately (barring a change in lifestyle).

I calculated that a 4% rate of inflation would increase this figure to a whopping $428,043 in 15 years.

Numbers seem big? I admit they are. Read this for more information: The Darwinian Doctor’s 13 Monthly Expenditures (with real numbers)

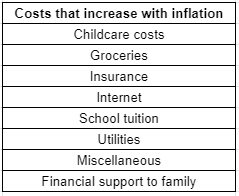

But when I revisited my calculations recently, I realized that I had made an error. Basically, not everything goes up with inflation.

Here are big expenditures that will likely increase with inflation, below.

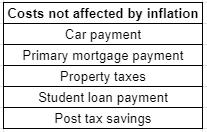

And here are costs that won’t go up with inflation.

Fixed debt and voluntary savings should not necessarily increase over time.

When I rechecked my projections with this new information, this fact alone shaved 1 year from our 15 year journey to financial freedom. But as you’ll see below, the transition to rental real estate has had an even greater effect.

The rental real estate empire

As a quick summary, in 2018, I bought my first rental property, and in 2019, I started a real estate investing course.

In 2020, our portfolio expanded to 10 doors.

In January of 2021, we closed on a 10 unit apartment building, growing our portfolio to 20 units. By late 2021, we hope to be generating over $6000/month in cash flow from these properties.

A faster road to moFIRE via cash flow?

So again we have the question: Am I accelerating my path to financial independence or not?

To answer this question, let’s talk a second about how I view cash flow.

To me, it’s a simple equation: $1 cash flow = $25 of investments

I alluded to this in my previous writing on cash flow, but if the 4% rule requires us to save 25 times our spending to fund expenditures, $1 of cash flow is therefore equivalent to $25 of savings.

Another way of thinking about this is that any cash flow you have at this moment can be used to pay your current expenditures. This directly impacts the amount of investments you have to put away to be considered financially independent.

My original 15 year plan to moFIRE

Below, you can see a graph where I calculated how long it should take us to get to moFIRE. We hit financial independence in 2034.

This plan is built on basic assumptions and aggressive, brute force saving:

- 8% annual compounded return

- 4% rate of inflation

- Hold expenditures steady

- Max out retirement accounts (~$106k/yr)

- Invest increasing amounts into taxable accounts every year (~$72k/yr, increasing by $6k annually)

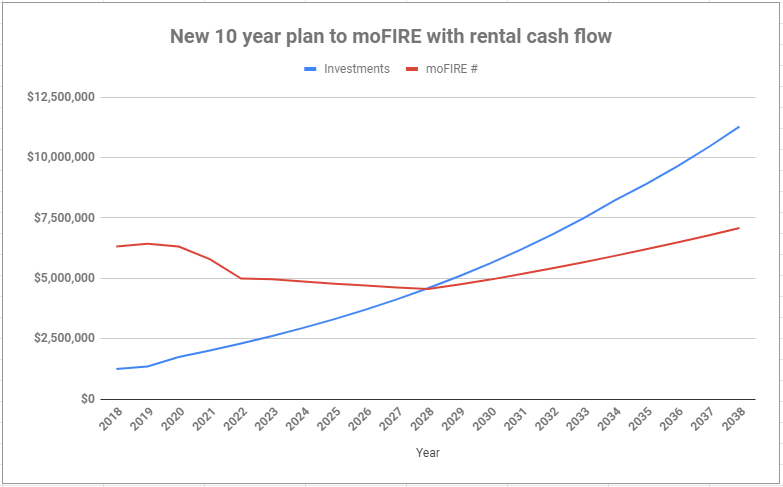

The new 10 year rental cash flow plan to moFIRE

This is my new graph to financial independence, taking into account my SMART goal of having $100,000 of cash flow from rental properties by 2025.

Now we hit moFIRE in 2028, five years faster than our inflation-adjusted 15 year timeline.

Here are the assumptions underpinning this graph:

- We continue to fully fund our retirement accounts and Roth IRAs (~$106k/yr)

- No further taxable brokerage account contributions

- All extra free cash flow gets diverted to real estate investment (~$70-90k/yr)

- Inflation continues at 4% annually

- No primary or rental home equity included in these numbers

We’re actually on pace to beat this timeline, but that was made possible by two big events in 2020: a taxable brokerage account sale ($200k) and taking a HELOC on our primary residence ($500k). Essentially, we re-purposed cash and equity we already had towards rental real estate.

From 2021 onwards, this graph assumes continued real estate investment from our free cash flow only.

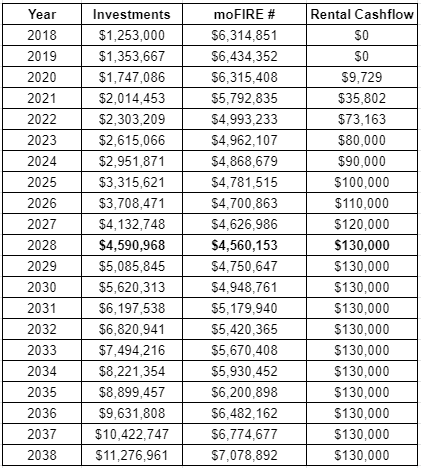

Here are the actual numbers, year by year:

As you can see, as our Rental Cash flow increases, our moFIRE # decreases. This is because the cash flow directly decreases the amount we have to save to be financially independent. As I noted above, each dollar cash flow replaces $25 that I otherwise would have to squirrel away into our savings vehicles.

Conclusion

In this post, I demonstrated how the cash flow from our rental real estate empire is accelerating our path to moFIRE. (morbidly obese financial independence, retire early).

By achieving approximately $10,000 of annual cash flow from real estate in 2020, we decreased our savings target by $250,000. This “moFIRE #” will continue to decrease as we increase our cash flow.

When we hit $100,000 annual cash flow by 2025 and increase that by $10,000 annually, we’ll hit moFIRE in 2028. This is 5 years faster that our inflation corrected 15 year plan to financial independence.

By these calculations, I’m definitely accelerating our path to financial independence. I still have some unanswered questions, like our average cost per cash flow dollar. Hopefully, I’ll have enough data to answer this question in a few months.

I apologize if you found this post boring or too numbers heavy. Every once in a while I like to force myself to crunch all of our numbers to make sure we’re on track. Without the accountability of publishing these blog posts for you, it’s too easy for me to make assumptions about my investing choices that aren’t backed up by reality.

As I mentioned, we’re on a faster cash flow trajectory than my assumptions above. It’ll be exciting to see how our actual progress compares to these numbers in a couple more years.

— TDD

What do you think? Do you find my projections realistic, or are there some mistakes I’ve made? If so, I want to hear about it!. Please comment below and subscribe to follow along!

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

Thank you for the great write up. Can you explain how your rental cash flow increases so rapidly between 2020-2027? Are you adding more properties or are you paying down the debt more aggressively?

Hi Nima, I’m adding more properties at a fairly rapid clip. Check this update out on my latest acquisitions: Buying a 10 unit apartment building | Anno Darwinii 1.5

Are you factoring rent increases into your projection, or is the increase in rental income solely from acquiring more properties? If you are factoring rent hikes in, how are you estimating them?

Hey AJ, great question. The increase in rental income I’ve projected is solely from acquiring more properties.

But the majority of my rental agreements have a 4% annual rent increase baked into the contract, so you’re right that I hope my rental income from my established properties will improve with time as well. I don’t put this into my calculations because I like to keep certain things conservative, to balance out my really optimistic projections on the growth of the rental portfolio.

With the debt fixed via long term mortgages, this is a good example of why rental portfolios often benefit from the buy and hold strategy. Income generally goes up, appreciation generally goes up, and debt stays fixed.

I’m obviously 11 months late to this post, but I stumbled onto your site today, and came across this post. I was drawn to it, as I had very similar revelations about investing, while managing a Pharma career. I initiated a similar real estate investing (in-conjunction with a separate low cost index stock market) strategy about 14 years ago. I had very similar FIRE projections (before FIRE was really talked about) and I’m happy to say, we out performed all of our initial projections and chose to retire early after just six years after purchasing our first rental units in 2009. We have now been essentially retired for over seven years. Our unit count is fairly steady now at 54 units, but we continue to search for new investment properties even in retirement. Our REI cashflow pays our retirement expenses several times over our original targets, and we’ve yet to tap our traditional market investments, which also continue to compound well untouched (we are still a few years away from 59.5 years old). Our net worth has risen much faster than expected due to rent increases and subsequent property valuations (tied to those rental increases) as well as phenomenal stock market investment returns over the same period.

Your plan is sound. There are a few minor road bumps to manage as you progress toward your goals: plan well for CAPEX as your properties will age, be flexible to “buy up” via 1031’s to offset that CAPEX requirement (this can be difficult due to 1031 time limitations and specific market availability). But I personally have found this investment strategy to be the easiest way to MoFIRE. Congratulations on your pursuit and success. Best of luck!

Thank you so much for taking the time to write up your experience! You had incredible timing in your entry into real estate, congratulations! It’s so good to hear that things worked out well. Your advice is sound with regards to CapEx. Bursting pipes and plumbing issues are a larger drag on our profitability than I expected.

One question for you — how did you decide when to 1031 exchange properties? I’ve already built up a good amount of equity in some of my properties, but it’s tough to know when to pull the trigger. I could sell four duplexes and trade into a larger multifamily, hopefully with Fannie Mae financing, but it’s difficult for me to know when it makes sense to do this.

thanks!

It really depends. The cost of executing a 1031 can be costly, so a quick cost analysis is be your best bet. I’ve focused on our properties that begin to age and eat into CAPEX a little faster. That tends to be properties that I’ve held for at least +8 to +12 years, so I’ve also built up some significant equity and captured significant depreciation/cap gains. If you’ve only held for a short period or have little equity or depreciation, then it’s highly unlikely worth the 1031 costs. (The costs for 1031’s can also fluctuate wildly depending on the group you are working with. Make sure you find a reputable group to work with, that has significant experience with 1031’s). Best of luck! I’m not a big poster, but I’ll probably be lurking around your site, now that I’ve found it. I may chime in (again) from time to time. Cheers!

Thanks a lot! This all makes a lot of sense. I’d love to hear more, so lurk away!

I find your post interesting w so much details to numbers and assumptions. You have made a wise decision to pivot into real estate. The missing piece to get to your MOFire state faster in 3-5 years is quite simple. Stop contributing to your retirement accounts! The market can be good or it can dip and it takes years to recover. Actually liquidate or get as much cash out of them as possible and go 100% into real estate. But you have to have a road map to follow. Take a course that will cost about $5-10k that will show you how, and exponentially increase your growth. I’m not affiliated w this company, but the guy who is the CEO has been teaching/mentoring people on how to do real estate the right way for 30 yrs and has about 50k members in all 50 states. He’s a self-made multi millionaire. You can listen to his podcast he tells funny stories about his own humble rise. You can sign up for a free 2 hr intro. They have connections to vendors etc. Then you can learn to do syndications from his classes or participate in syndications that other members put together. Most of his members achieve FI within 3-5 years, he claims. I first found out about him because he’s so rich he bought out the prime 6pm time slot on my local talk radio station about 2 yrs ago, so I listened to him almost daily for 2 yrs on drive home. I invest passively in syndications and don’t do the active stuff. You can check out the podcast also, there’s 2 versions out there be sure to listen to the one called Del Walmsley Radio Show.

Thanks for the comment Keith! I’ve tried to have the best of both worlds with both stock and real estate investing, but you’re right that it has slowed my progress towards financial independence. And my retirement funds are certainly money jail. I’ll have to write about this soon.