In this post, I introduce you to cap rates—what they are, why they matter, and how you can use them to make smarter real estate investments.

Why Are You Here?

Let’s start with a simple question: Why are you reading this?

If I had to guess, you’re after the same things I was when I started my financial freedom journey—less reliance on your day job, more passive income, and maybe even a legacy for your kids. The ultimate dream? Time freedom. The ability to choose how you spend your days, rather than having your schedule dictated by your employer.

For many high-income professionals, the traditional path to wealth looks something like this:

- Work hard

- Earn a good salary

- Invest in stocks

- Retire after 30+ years

But what if you want to accelerate that timeline? What if you want to hit your financial goals in 10 or 15 years instead of waiting three decades?

That’s where real estate comes in.

I’ve always been a data guy, and when I started crunching the numbers between stocks and real estate, the math told me something surprising—real estate offered higher returns, better tax benefits, and more control. But to make smart investments, you need to understand how properties are valued.

And that brings us to today’s topic: capitalization rates, or “cap rates.”

Stocks vs. Real Estate: A Quick Recap

Before we dive into cap rates, let’s talk about why real estate often outperforms stocks—especially for high-income professionals like doctors.

Stock Market Returns

The average return of the stock market over time (via index funds like the Vanguard Total Stock Market Index) is around 8-10% annually. That’s a solid return. If you’re lucky (or very skilled), you might pick a winning individual stock and blow that number out of the water. But you could also pick the wrong stock and lose big.

Real Estate Returns

When investing passively in real estate—such as through syndications or private equity deals—the average returns are closer to 15% per year (at least in the current environment). And when you factor in tax benefits, appreciation, and leverage, the real returns can be even higher.

Consider this:

- $100,000 invested in stocks at 8% annual returns grows to $931,000 in 30 years.

- $100,000 invested in real estate at 15% annual returns grows to $5.7 million in 30 years.

Even better, if you invest an additional 50,000 per year into real estate (instead of just letting your initial investment sit), you could hit $1.2 million in just 10 years and $25 million in 30 years.

That’s the power of compounding at a higher rate of return.

But can you really get 15% returns in real estate?

Yes—you just need to understand how to evaluate deals.

Cap Rates: The Secret to Evaluating Investment Properties

What Is a Cap Rate?

“Cap rate” is short for capitalization rate, and it’s one of the most important metrics in real estate investing.

It tells you how much return a property generates based on its income relative to its value. The formula is simple:

Cap Rate =

Net Operating Income (NOI)

Property Value

Where:

- Net Operating Income (NOI) = Total rental income minus expenses (excluding mortgage payments)

- Property Value = The price you pay for the property

For example, if a property generates $100,000 in NOI and is worth $1,000,000, the cap rate is:

$100,000

$1,000,000

= 10%

This means that if you bought the property in cash (no mortgage), you’d get a 10% annual return on your investment.

What Do Cap Rates Tell You?

1. Higher Cap Rates = Higher Risk, Higher Reward

A higher cap rate (e.g., 8-12%) typically means the property is in a less desirable area or has higher risks (older building, higher vacancy rates, etc.).

For example:

- A 10% cap rate might be in a C-class neighborhood with higher tenant turnover and maintenance costs.

- A 3-4% cap rate is common in premium markets like New York City or Los Angeles, where property values are high, but rent is relatively low.

2. Lower Cap Rates = Safer, But Lower Returns

A lower cap rate (e.g., 3-5%) usually means:

- The property is in a prime location with strong long-term appreciation.

- The demand is high, leading to lower cash flow but greater stability.

In cities like New York or San Francisco, investors might accept a low cap rate because they believe the property will appreciate significantly over time.

How Investors Use Cap Rates

1. Comparing Properties

If you’re deciding between two apartment buildings and one has a 6% cap rate while the other has a 9% cap rate, the 9% cap rate property offers a better cash return—but may come with higher risks.

2. Estimating Property Value

If you know a property’s NOI and the average cap rate for similar properties, you can estimate its value.

Example:

- The average cap rate in your target market is 5%

- The property generates $200,000 in NOI

- Estimated value = $200,000 ÷ 0.05 = $4,000,000

3. Determining Whether a Deal Makes Sense

If your mortgage interest rate is higher than the cap rate, you’re in trouble.

Example:

- If you’re buying at a 6% cap rate, but your loan has an 8% interest rate, you’re likely to lose money each month.

- But if you can improve the property (raise rents, lower expenses) and increase the NOI, you might be able to push the cap rate higher and create value.

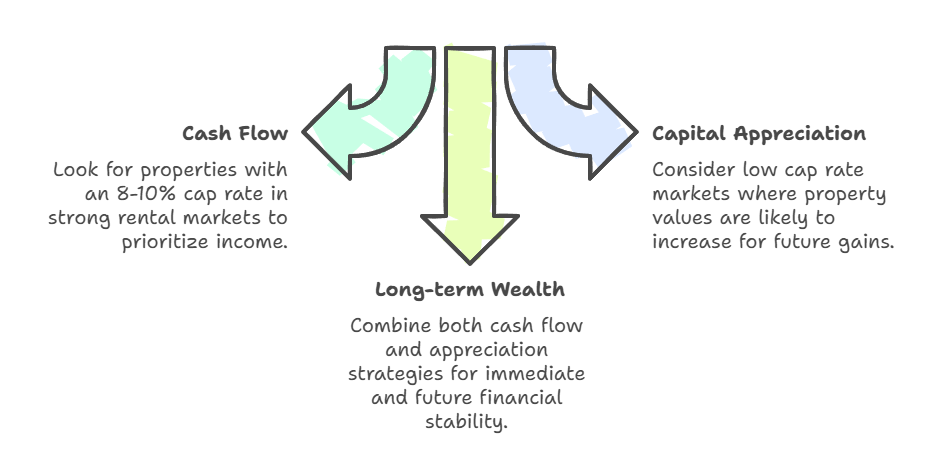

Cap Rates and Your Investment Strategy

So, what cap rate should you be looking for?

- If you want cash flow, look for properties with an 8-10% cap rate in strong rental markets.

- If you want capital appreciation, consider low cap rate markets where property values are likely to increase.

- If your goal is long-term wealth, consider a mix of both—cash flow for immediate income, and appreciation for long-term gains.

And don’t forget: Cap rates aren’t the only factor. Tax benefits, leverage, and forced appreciation all play a role in your real estate returns.

Final Thoughts: How to Take Action

Understanding cap rates is key to making smart real estate investments. But cap rates alone don’t tell the full story—you need to consider the location, property condition, financing, and long-term strategy.

If you’re serious about building wealth through real estate, investing passively in high-quality deals can be a game-changer. That’s exactly what we do at Cereus Real Estate—we help busy professionals invest in cash-flowing properties without the headaches of being a landlord.

So what’s next?

- Start tracking cap rates in your target markets.

- Learn how NOI and expenses impact property value.

- Consider passive investing if you don’t want to manage properties yourself.

Financial freedom isn’t a dream—it’s a decision. Let’s get there together.

Daniel Shin, MD

The Darwinian Doctor

Want to learn more about how real estate can transform your financial future? Visit Cereus Real Estate to see how we’re helping physicians achieve passive income and financial independence.

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions