This is the real data from my tax returns that show how much I paid in federal taxes as a physician real estate investor on the road to financial independence.

This post may contain affiliate links.

Introduction

When I awoke to the reality of my golden handcuffs as an attending physician in 2018, I made a goal to be financially independent within 15 years. After a short while, I realized that an aggressive tax mitigation strategy had to be a large component of this plan. After all, for high income professionals, taxes are going to be your biggest expense by far.

As a physician, this is one of the main reasons why I have progressively turned to real estate investing as a central component of my tax reduction plan.

This post lays out some of the ways that real estate investment can be part of a great reduction tax strategy: Tax Benefits | Why I’m Investing In Real Estate Over Stocks.

The power of depreciation

One of the main reasons why real estate is so tax efficient is depreciation. I call depreciation the “stuff wears out deduction.”

Essentially, if you own real estate, you’re allowed to claim a certain percentage of the value of the building as a paper loss every year. This is a tacit acknowledgement by the IRS that buildings suffer from wear and tear over time.

In some cases, you can even accelerate those losses and push a lot of them into year one of ownership. This is a process called “accelerated depreciation” and requires something called a cost segregation. I discuss this in detail here: Amazing Tax Deductions from your Short Term Rental.

As I explain in the post, for people that spend the majority of their time in a day job, the most powerful tax mitigation strategies might involve a short term rental. If you’re going for long term rentals, you can still benefit from tax savings. However, these paper losses aren’t deductible against your active income unless you can achieve real estate professional status.

Need someone to help you with a cost segregation? Check out my recommended providers here!

Real life data is the best data

I think in general, real life data is the most helpful to demonstrate a concept in action. Therefore, below I’m going to show how much I paid in federal taxes as a physician real estate investor on the road to financial independence.

For the purposes of this post, I’m going to stick to my federal taxes. It’s simpler to understand and more universally applicable. Also, in 2022 my family moved from California to Tennessee, which complicates our return.

The origin of our depreciation

In 2022, I purchased a short-term rental in Broken Bow, Oklahoma. This is a beautiful cabin in the middle of a wooded area just minutes from the town and Broken Bow lake.

I also embarked on a significant renovation of my second home in Palm Springs, which was I was able to recognize as a tax deduction through a “partial asset disposition” study.

(As long as I own these houses, you can rent them here!)

$473,000 of deductions

From the study, we were able to recognize an additional $192,532 of previously un-depreciated basis for the Palm Springs property. For our Broken Bow cabin, we were able to recognize $280,804 of depreciation from our cost segregation.

In total, this led to around $473,000 of deductions related to these two properties in 2022. We were able to accelerate the vast majority of these into our 2022 tax year to offset our active income. These paper losses caused a big drop in my marginal (top) tax rate, as well as my effective (final) tax rate.

How much we paid in federal taxes

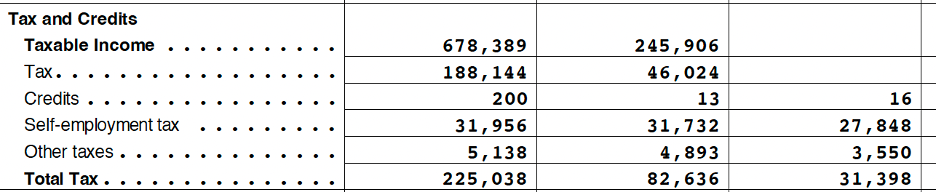

Overall, our real estate activities (plus other deductions) almost completely cancelled out our federal tax liability in 2022. In the end, we ended up paying about $30,000 in federal income taxes in 2022 on a gross income of around $675,000* for the year.

- Total Federal Tax paid: $31,398

- Federal Marginal tax rate: 10.0%

- Federal Effective tax rate: 4.7%

This is a big improvement from the year prior, where we still paid over $80,000 to the IRS. Even that was a marked improvement compared to 2020, when we paid almost a quarter million dollars in federal taxes.

*Note: In 2022, my family moved from Los Angeles to Memphis, so $675,000 reflects nine months of earning for me and almost a full year’s earning for my wife at our day jobs.

Since we had already paid about $67,000 of tax payments to the IRS through paycheck deductions, we ended up getting a $35,000 refund in 2022 related to our federal taxes.

Other deductions

Of course, real estate didn’t provide all of our deductions in 2022. We also claimed a myriad of other deductions related to our other income from our regular employment. Here’s just a few of them:

- Retirement contributions

- Home office deduction

- Medical conferences

- Business conferences

- Licensing fees

- Charitable donations

Did the tail wag the dog?

There’s an important saying in investing: “Don’t let the tax tail wag the dog.” It basically means that you shouldn’t buy an investment only for the tax savings. It should be a sound investment by itself.

When it comes to the short term rentals, I think I was a little guilty of this. As you can see, the tax savings from my investments were huge, legally saving us about $200,000 of federal taxes in 2022.

However, these investments were a big deviation from my initial plan to use long term rentals to provide consistent, hands-off passive income. Short term rentals are the opposite of “hands-off.” They take an incredible amount of time and effort to run effectively in the best of circumstances.

In the worst of circumstances, they can be expensive liabilities.

As I discussed in this post about Palm Springs short term rental regulations, one big problem I ran into was a temporary suspension of our rental permit due to paperwork errors. Due to this snafu, our beautiful rental essentially sat empty for about 6 months in 2023 during the height of the rental season.

This all led to about a $75,000 loss from this property in 2023. When it comes to real estate, maintenance costs such as property taxes, utilities, and mortgage payments don’t stop just because the property is un-rentable.

Luckily, the property is up and running again now as a profitable rental, but it’s a good cautionary tale.

Looking to the future

Since 2022, I’ve steadily refocused my investing lens on multifamily residential real estate. This led to my own investments into real estate syndications and the launch of Cereus Real Estate, which is bringing passive investment opportunities to high income professionals. A physician who works full time can still enjoy tax savings from passive real estate, though it’s not as dramatic as what you can get from active real estate investing.

Read more: 5 Reasons Why I’m Finally Investing in a Real Estate Syndication

I’m prepping an Anno Darwinii post to discuss these developments – make sure to subscribe to my newsletter so you get notified about that when it’s released!

Conclusion

I hope you enjoyed this look into my taxes as a physician real estate investor. Too much of the time, we hear advice without the actual data to show that advice playing out in the real world. I hope this shows you the power of using real estate as a tax mitigation strategy!

A good tax mitigation strategy is essential for high income professionals on the path to financial freedom. Real estate is one of the most tax-efficient investment classes because the government wants to promote investment into this sector. After all, real estate investors create and maintain our nation’s housing supply!

If you want to learn more about using real estate to supercharge your journey to financial freedom, make sure to subscribe to my free newsletter below!

Daniel Shin, MD

The Darwinian Doctor

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions