Unlock the hidden tax benefits of real estate syndications and take your wealth-building to the next level.

If you’re anything like me, taxes are one of your least favorite expenses. So, wouldn’t it be great if we could legally keep more of our hard-earned money?

Well, here’s the good news: real estate investing—especially through syndications—offers some incredible tax advantages that can help you grow wealth faster while minimizing what you owe to Uncle Sam. And no, this isn’t some shady offshore account scheme—it’s all completely legal.

In this post, we’ll break down exactly how real estate syndications can reduce your tax bill while allowing your wealth to grow. We’ll cover:

- Depreciation: The “stuff wears out” tax deduction

- Tax-deferred growth: How real estate investments grow tax-free (until you cash out)

- Tax-efficient distributions: The cash flow that (usually) isn’t taxed

- Long-term capital gains: Why real estate beats W2 income every time

- 1031 exchanges: The ultimate way to defer taxes indefinitely

- K-1 losses: How paper losses can offset other investment income

Let’s dive in.

Depreciation: The “Stuff Wears Out” Tax Deduction

Depreciation is the secret sauce of real estate investing. It’s the IRS’s way of acknowledging that buildings don’t last forever—paint peels, carpets wear down, and appliances break. Because of this, the government allows you to deduct a portion of a building’s value from your taxable income every year.

How it Works

- Residential real estate depreciates over 27.5 years, meaning you can deduct about 3.6% of the property’s value per year.

- This depreciation is a paper loss, meaning you’re deducting an expense that doesn’t actually come out of your pocket.

- If you invest in a real estate syndication, you’ll receive these benefits without having to deal with the headaches of being a landlord.

Bonus Depreciation and Cost Segregation

Want to supercharge your tax savings? That’s where cost segregation studies and bonus depreciation come in—two powerful tools that work together to front-load tax benefits.

A cost segregation study breaks down a building into its individual components—like electrical wiring, appliances, and flooring—so that instead of depreciating everything over 27.5 years (residential) or 39 years (commercial), you can accelerate depreciation on certain parts of the property over 5, 7, or 15 years.

Here’s where it gets even better: bonus depreciation allows you to immediately deduct most (or all) of those shorter-lived assets in year one, rather than spreading the deductions over time.

For example, in the Hampton Meadows syndication deal, investors who put in $50,000 received $14,000 in passive paper losses in the first year alone! This wasn’t magic—it was a combination of cost segregation identifying fast-depreciating assets and bonus depreciation allowing investors to write them off immediately.

Important note: Bonus depreciation used to be 100% (meaning you could deduct the full amount in year one), but it’s been phasing out since 2023:

- 80% in 2023

- 60% in 2024

- 40% in 2025

- 20% in 2026

- 0% in 2027 (unless laws change)

So while this strategy is still powerful, the size of these upfront tax deductions depends on when you invest.

(There is a good possibility that bonus depreciation might go back up, but it really depends on tax legislation that may or may not be passed in 2025.)

Tax-Deferred Growth: Let Your Money Compound

One of the biggest benefits of investing in real estate syndications is that your investment grows without being taxed until you sell.

Here’s why this matters:

- Real estate increases in value over time through appreciation, rent increases, and inflation.

- Unlike W2 income, where the IRS takes a cut every paycheck, real estate gains aren’t taxed until they’re realized (when the property is sold).

- You can even strategically plan when to sell in order to minimize your tax burden.

This is why wealthy investors love real estate—your money grows, but your tax bill stays low.

Tax-Efficient Distributions: Cash Flow That (Usually) Isn’t Taxed

In a successful syndication, investors receive quarterly cash flow distributions. But here’s the fun part—these payments are often tax-free because they are classified as a return of capital rather than taxable income.

This means:

- You receive passive income throughout the investment period.

- You may not owe taxes on those distributions (depending on the deal structure).

- You still get the full benefit of appreciation when the property is sold.

Think of it like getting dividends from a stock—except in many cases, you don’t have to pay taxes on them right away.

Long-Term Capital Gains: Why Real Estate Beats W2 Income

When a real estate syndication sells, investors receive a lump sum profit, which is taxed as a long-term capital gain (if held for more than a year).

Why is this a big deal? Let’s compare tax rates:

- W2 income: Taxed at rates as high as 37% (federal).

- Long-term capital gains: Taxed at a maximum of 20%.

This means that a doctor, engineer, or any high-income professional can cut their tax rate nearly in half just by earning income through real estate instead of their job.

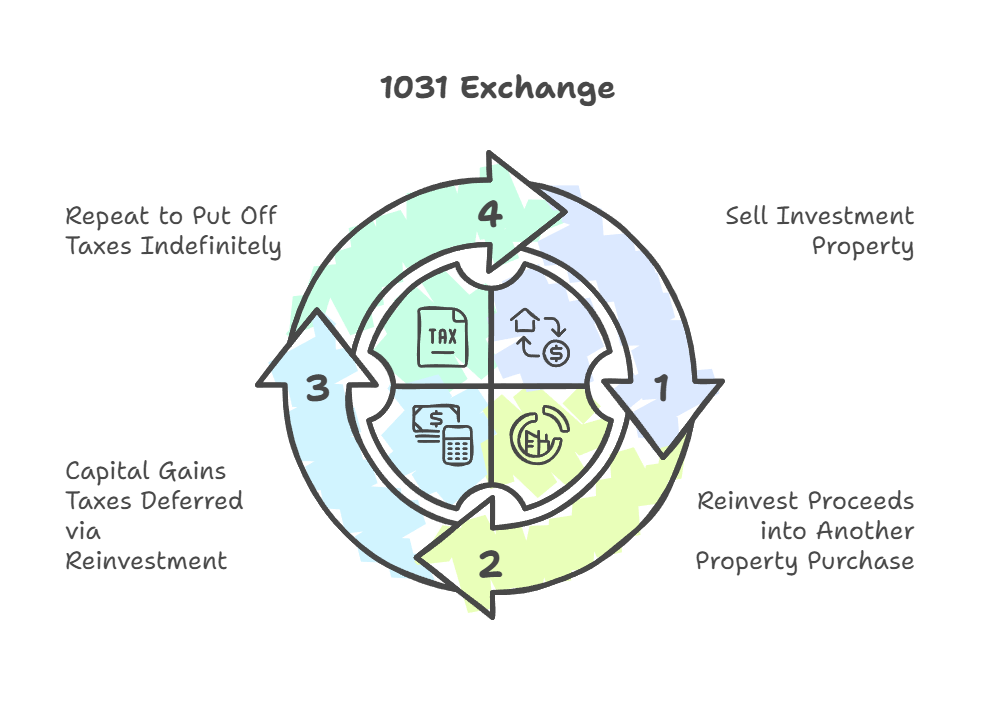

1031 Exchange: The Ultimate Tax Deferral Strategy

OK, we’ve discussed real estate syndications offer inherent tax benefits, but what if I told you there’s a way to never pay capital gains taxes at all?

Enter the 1031 exchange—a strategy that allows investors to roll profits from a real estate sale directly into another property, deferring taxes indefinitely.

How It Works:

- You sell an investment property.

- Instead of cashing out, you reinvest the proceeds into another real estate deal.

- You defer paying capital gains taxes until you eventually sell without doing another exchange.

- Many investors keep doing 1031 exchanges for life, avoiding taxes entirely.

In some syndications, 1031 exchanges are an option, but you’ll need to check with the deal’s sponsors to ensure the structure allows for it.

K-1 Losses: Use Paper Losses to Offset Passive Gains

If you’ve ever invested in a real estate syndication, private equity deal, or even some medical partnerships, you’ve likely received a K-1 tax form.

K-1 losses are powerful tax tools because they can offset other K-1 income.

For example:

- You earn $100,000 from a surgery center investment (reported on a K-1).

- You also invested in a real estate syndication that gives you $80,000 in passive paper losses.

- Your taxable income drops to $20,000 instead of the full $100,000.

For high-income professionals, this can lead to massive tax savings.

*Make sure to check these assumptions with your CPA! I’m not a tax professional.*

Real Estate Professional Status: Can You Use These Losses Against W2 Income?

It’s time to make a quick but important point about how the tax benefits of syndications relates to your W2 income.

A common misconception is that real estate losses can offset W2 income. Unfortunately, that’s not the case—unless you qualify as a Real Estate Professional (REP).

To achieve REP status, you must:

- Work 750+ hours per year in real estate.

- Spend more time in real estate than any other job.

For most full-time professionals, this is nearly impossible. Even as a doctor doing part-time locum tenens work, I couldn’t qualify in 2023 because I didn’t document my hours well enough!

So unless you or your spouse are fully committed to real estate, these tax benefits will apply only to passive income—not your W2 salary. That doesn’t mean that the tax benefits of real estate syndications aren’t powerful — they are! Their benefit just tends to apply more to future income.

The Key to Wealth: Always Be Investing

I hope you now have a better understanding of the tax benefits of real estate syndications. The real magic of these tax benefits isn’t in just one real estate investment—it’s in consistent reinvestment.

By rolling gains from one deal into another, you can:

- Continuously defer taxes.

- Use new depreciation losses to shelter old gains.

- Accelerate your wealth-building journey.

The Bottom Line

Real estate syndications offer some of the most powerful tax advantages available to investors. From depreciation to long-term capital gains treatment, these benefits allow you to keep more of your money while compounding your wealth.

And if you’re ready to take advantage of these benefits, check out Cereus Real Estate—my real estate investment company—where we help investors like you achieve financial freedom through passive investing.

Because remember—financial freedom isn’t a dream, it’s a decision. Let’s get there together.

Daniel Shin, MD

The Darwinian Doctor

Experience the financial benefits of real estate without dealing with the headache!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions