In today’s post, I’ll walk you through the painful process of getting a mortgage, and why I think this is a good thing.

In the last edition of Anno Darwinii, I outlined the rapid expansion of our real estate empire in the last 6 months. To recap, in 2021 we bought two small apartment buildings and a vacation home. This added 18 more units to our portfolio, bringing us to a grand total of 28 units. One of the more exhausting parts of this expansion has been the mortgage process.

At one point, I was putting in multiple mortgage applications at once while collecting quotes. I spent many nights fighting back yawns, downloading dozens of bank documents, cursing the underwriters and their insatiable curiosity.

But now with the clarity of hindsight, I’m glad that the mortgage process was so painful. Curious why? I’ll sum it up with four words: mortgage crash of 2008.

To explain, let’s divide this post into two parts:

- Why getting a mortgage is so painful

- What they’re trying to avoid

Why getting a mortgage is so painful

The ironic fact about mortgage applications is that the more assets you have, the more painful the application process is.

The simplest mortgage applicant is a well paid employee with a large cash pile and perhaps one credit card. That’s it. For this lucky person, the application process will be a breeze!

But in reality, most people applying for a mortgage have something more like this:

- Auto loans

- Student loans

- Four credit cards

- Retirement accounts

- Multiple subscription services

- Savings and checking accounts

If you’re a real estate investor, you can add on these things as well:

- HELOC(s)

- Multiple mortgages

- Business credit cards

- Business checking accounts

Each additional wrinkle to your financial portfolio will add additional scrutiny to your mortgage application.

Basically, the more assets you have, the more documents you can expect to download, sort, and send to the bank. This can be a painful process.

The standard mortgage application

The standard mortgage application isn’t so bad on its own. It’s time consuming, because you must list all your essential identifying information, like address, social security numbers, and employers. You’ll also list your basic financial profile, with the approximate balance of your assets and liabilities.

If you have real estate, you’ll list information about each property, including your closing documents and any associated mortgage information. You also have to consent to a hard credit pull. Expect to spend at least a few hours on this process, but it’s fairly straightforward.

Related post: The fastest way to improve your credit-score

The lender will process your documents for a while. And then, when you’ve crossed enough hurdles to get your application to the underwriters, the mortgage hell truly begins.

Underwriting hell

Prepare to spend dozens of hours over the next few weeks doing this:

- Sending 2 years of tax returns

- Sending 2 months of pay stubs

- Sending 2 months of bank statements (all pages!)

- Writing letters of explanation about credit inquiries and cash transfers

- Sending duplicate documents because the underwriters lost your files

- Sending everything again because the underwriting process takes so long that they need to refresh the documents

The underwriters are analyzing your data to calculate your debt to income ratio, but also to see more holistically how risky it is to extend credit to you.

Along the way, they’ll torture you enough to make you regret applying for a mortgage in the first place.

What they’re trying to prevent

In all fairness, there is a good reason why lending standards are now so annoying. It’s to avoid another mortgage fueled crash like we saw in 2008.

After too many sub-prime NINJA loans (no income, no job, no assets), the mortgage bubble burst when over two million people lost their houses to foreclosure in 2008. The recession that followed was the worst since World War II.

Basically, a lot of people who bought homes pre-2008 never should have been approved for credit. When they stopped being able to pay their mortgages and defaulted, this started a chain reaction that brought America, then the world, to its knees.

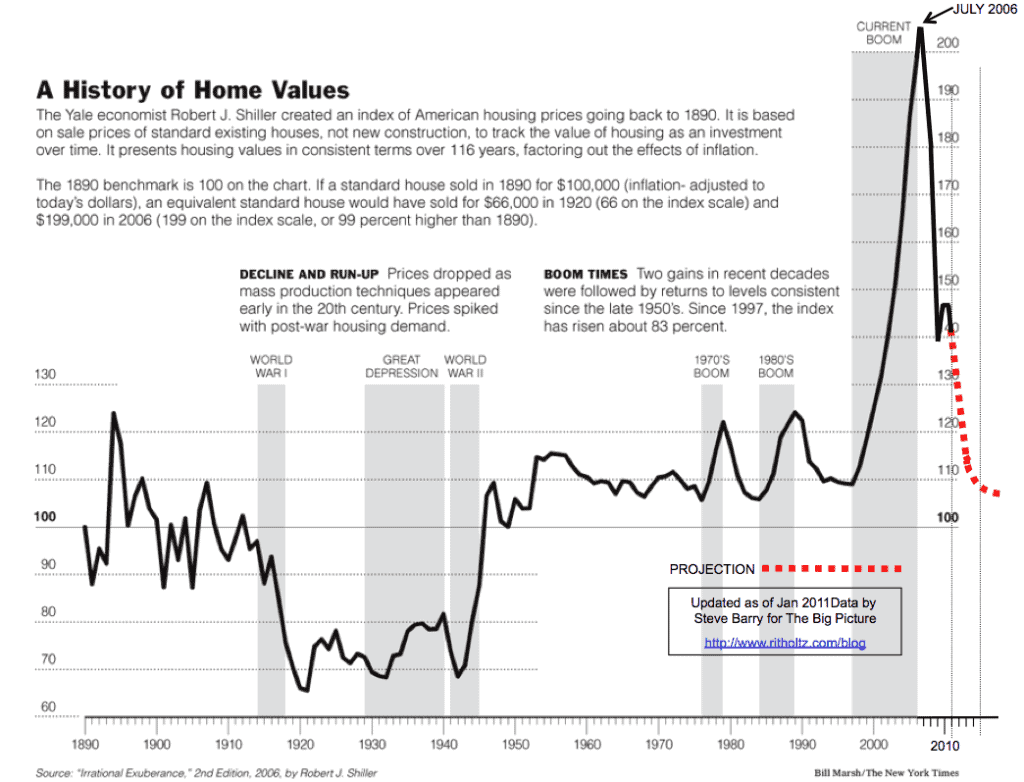

As you can see below, this essentially halved home prices across the United States. Here’s a graph showing the Case Shiller index from 1890 through the crash immediately after 2008. The only other time in history that saw such a drop in home prices was after World War I.

(Interpreting the Case Shiller index: A standard house in 1890 is 100 on the scale. A standard house being a 200 on the scale means that it sold for 2 times the amount it did previously. As far as I can tell, it’s inflation adjusted, so it normalizes the worth of money and is a more accurate representation of the value of homes in general.)

The economic devastation caused by the Great Recession went far beyond home prices. The unemployment rate in the US doubled to over 10%. Overall, the ripple effects led to a loss of over $2 trillion of global economic growth.

Conclusion

So in summary, getting a mortgage can be really painful. But as we discussed, it’s probably a good thing, since the alternative is a repeat of the mortgage crisis of 2008.

So request away, dear underwriters. I’ll keep on sending you my documents, as long as you do your job and prevent another Great Recession.

–TDD

Do you have a painful mortgage story? Comment below and please subscribe to my weekly newsletter!

Perhaps you’re more of a Facebook type?

Are you a physician, spouse, or professional and you’re interested in using Real Estate to gain financial freedom? Join us in our Facebook group and accelerate your journey!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

Right on. This is exactly what I tell myself when applying for loans. It is also what I think about when analyzing this market… it is only natural for us who lived through the 2008 housing crisis to fear a repeat but the standards are far different… now a correction may still occur but it is very unlikely to be a 2008 level event 😉

Agree! Aside from (another) catastrophic world event like World War I, hopefully these high lending standards are keeping us safe from another 2008 crisis for the time being.

I like that it’s more painful to get a mortgage now than before where if you just had a pulse, the banks lent you money.

However, I feel like they should get rid of the “require W-2 income” rule because that feels too restrictive. But then again, maybe that’s why I don’t get paid the big bucks.

The W2 income preference is definitely a problem for business owners and side gig workers. The banks will accept 1099 or other business income, but as you probably know, they’ll need 2 years of proven income. This bar is much higher than for W2 workers, who just need employment verification and two months of paystubs.

With access to a wide range of mortgage products, a broker is able to offer you the greatest value in terms of interest rate, repayment amounts, and loan products.

I appreciate your candid account of the mortgage process and the reasoning behind its complexity. It’s eye-opening to realize that the pain and hassle of collecting and submitting numerous documents are actually necessary precautions to prevent another mortgage crash like the one in 2008. Your explanation of how lending standards have evolved to avoid risky loans and subsequent foreclosures provides valuable context. The graph illustrating the significant drop in home prices during that time is a stark reminder of the economic devastation caused by the Great Recession.