Traditional financial advice works well for many people, but physicians follow a very different path. Here’s why that difference often changes the way we think about wealth, investing, and financial flexibility.

One of the more interesting things about getting older is realizing that your goals don’t always change as much as your definition of success does.

I still enjoy medicine, I still enjoy investing and I still enjoy building businesses and taking on projects that challenge me intellectually. If anything, I’m probably more ambitious today than I was fifteen years ago. What has changed is how I evaluate progress.

Earlier in my career, I paid close attention to outcomes. Every investment and every business decision felt important. Every opportunity carried a certain weight because I was trying to determine, as quickly as possible, whether I was making the right choices. If something worked, it felt like validation. If it didn’t, I wanted to understand immediately what I had missed.

Looking back, I think a big contributor to this phenomenon was that I was coming from a place of scarcity.

It was early in my career as a surgeon, when my bank account was small, my debt was large, and my free time was limited. So every investment decision took on outsized importance.

Over time, as my wealth and control over my time grew, I found myself becoming less interested in individual outcomes and more interested in the structure behind them. I paid more attention to the people involved, the incentives driving decisions, the downside risk if things didn’t go according to plan and whether something was likely to remain durable over the long run.

Along the way, I’ve come to appreciate that good decisions don’t always produce immediate rewards and bad decisions occasionally get lucky.

This was a change that came about as a side effect of more experience and more abundance. I was able to pay attention to the bigger picture, rather than the noise.

This change has made me a better investor and fund manager.

I believe that many physicians follow a similar evolution in their own financial journey, but perhaps for slightly different reasons.

The Advice Isn’t Wrong

Most physicians eventually receive some version of the same financial playbook: save consistently,maximize retirement accounts, invest in broadly diversified index fund and stay patient and allow compounding to work over time.

It’s sensible advice. In fact, for many people, it’s probably exactly the right advice.

The challenge is that physicians often arrive at the financial starting line under very different circumstances than the people those recommendations were originally designed for.

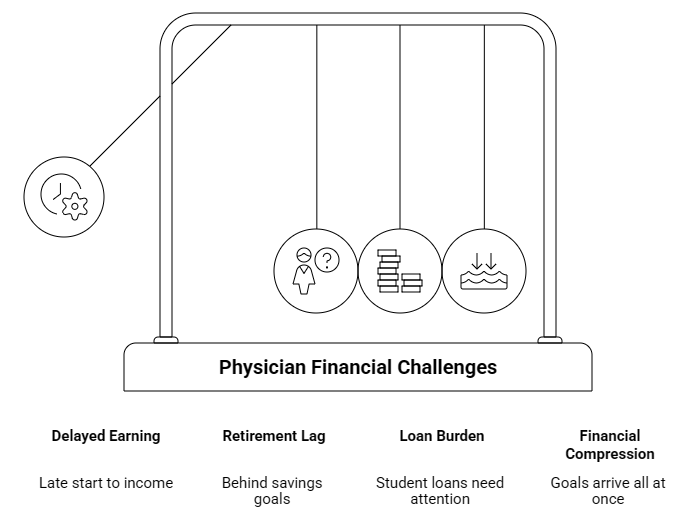

Medicine follows a fairly unusual timeline. While many of our professional peers are beginning careers, contributing to retirement accounts, buying homes and steadily building wealth throughout their twenties, most future physicians are still in training. The years that many professionals spend accumulating assets are often spent accumulating knowledge, experience and, unfortunately, a significant amount of debt.

Eventually, attending-level income arrives. From the outside, it can look like the financial challenges are suddenly over. After all, physicians earn high incomes and high incomes solve a lot of problems. But what often goes unnoticed is that many doctors are stepping into that income after a decade or more of delayed earning. Retirement savings may be behind where they’d hoped. Student loans still need attention. Families are growing. Homes are being purchased. Financial goals that might have been spread across many years for other professionals often arrive all at once.

I remember feeling this tension myself during my early attending years. I was grateful for the opportunities medicine had provided and fully aware of how fortunate I was to be earning a physician’s income. At the same time, there was a persistent feeling that I was trying to compress years of financial planning into a much shorter window.

This compressed earning window, in my opinion, makes it even more important for us to carefully consider risk, timeline, and reward potential. When you start earning a real paycheck at 35 years of age in a punishing career, perhaps a 30 or 40 year timeline isn’t the right way to frame your ideal financial journey.

When More Income Stops Being the Answer

One of the great financial advantages of medicine is the ability to generate income through your own effort. If you want to earn more, there are often clear paths available: work additional shifts, take more call, increase productivity and see more patients. The connection between effort and income is often direct and predictable.

For a long time, that’s exactly how I thought about financial progress. In my first couple of years, I gladly took on more call and more overtime pay. Especially within the employed model where I worked, that was really the only way to make more money.

And it did work. The big income allowed me to start paying back my student loans and save money to start my investment journey.

Medicine gave me stability, flexibility and opportunities that I never take for granted. I’m grateful for it to this day.

But at some point, I started noticing that my questions were changing.

Earlier in my career, most of my financial goals revolved around accumulation. I wanted to save more, invest more and build more. Those goals were important and they still are, but as the years passed and my wealth grew, I found myself thinking more about how I wanted my life to feel on a day-to-day basis.

- How much control did I have over my schedule?

- How much of my time felt intentionally allocated versus committed by default?

- Was I building a career that supported the life I wanted outside of work, or was I constantly rearranging the rest of my life around my career?

Those questions didn’t appear overnight. They emerged gradually, almost quietly. And once they appeared, they became difficult to ignore.

I suspect many physicians eventually arrive at a similar point. There comes a stage where earning more money no longer solves the problem you’re trying to solve. The issue isn’t income. The issue is flexibility. It’s the realization that a high income and a high degree of control over your time are not necessarily the same thing.

That distinction became increasingly important to me over time, and is one of the main reasons why I increasingly gravitated towards real estate.

A Different Definition of Wealth

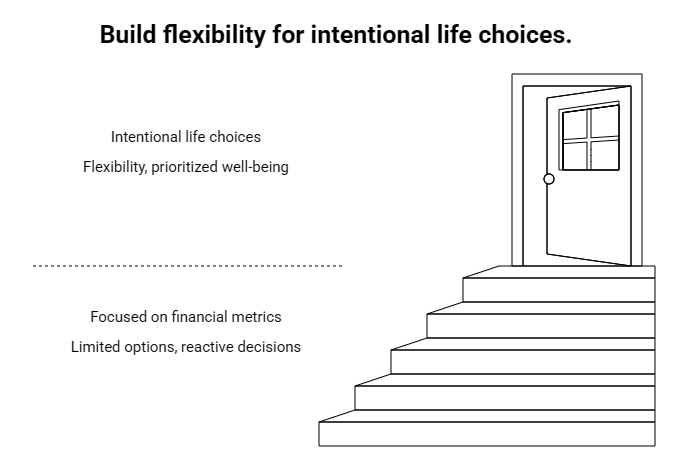

Somewhere along the way, I stopped viewing wealth primarily as a number and started viewing it as a source of optionality.

When we’re younger, it’s natural to focus on numbers. Net worth, income, investment returns: those metrics are easy to measure and they’re useful in many ways, but they don’t always capture how someone actually experiences their life.

Some of the people I’ve admired most over the years weren’t necessarily the wealthiest people I knew. They were often the people who seemed to have the greatest degree of intentionality. They had built lives that gave them flexibility. They could make decisions thoughtfully rather than reactively. They had the ability to prioritize family, health, travel, meaningful work, or personal interests without feeling constrained by every financial decision.

That’s a different kind of wealth. And unlike income or net worth, it’s not always visible from the outside.

Looking back, I think this is one of the reasons traditional financial advice can sometimes feel incomplete for physicians. Most financial advice is designed to maximize long-term wealth creation, which is an important goal. But many physicians are also searching for something else. They’re trying to create a life that feels sustainable. They’re trying to build enough flexibility that future decisions can be made from a position of choice rather than necessity.

Those are related goals, but they’re not exactly the same.

Why Real Estate Changed My Perspective

For me, real estate investing became one of the vehicles that helped shift my thinking.

Not because I believed it was a magical solution and, certainly, not because I think every physician should abandon traditional investing strategies in favor of real estate. I still believe broad market investing has an important place in a well-rounded financial plan.

What real estate introduced was a different perspective on ownership.

Like many physicians, most of my income had always been tied directly to my work. I practiced medicine and I was compensated for that effort. It was a straightforward and highly rewarding arrangement. Real estate was one of the first areas where I began thinking differently about how income could be generated. Instead of relying entirely on personal effort, I became increasingly interested in ownership, cash flow, and asset-based income.

At first, I was drawn to the numbers. The tax advantages and the potential returns were appealing. But over time, I realized the deeper impact was psychological.

As my investments grew, I found myself making decisions differently. I became less reactive and I felt less pressure to maximize every opportunity that came my way simply because it existed. The presence of additional income streams didn’t dramatically change my life overnight, but it gradually created more room to think, plan and make decisions with greater intention.

The most meaningful change wasn’t financial. It was the growing sense of optionality.

The Question Behind the Question

Over the years, I’ve had countless conversations with physicians about investing, financial independence and building wealth. On the surface, those conversations are usually about asset classes, returns, taxes, or investment strategies.

But I don’t think that’s what they’re really about.

More often, I think physicians are trying to answer a deeper question. They’re trying to figure out how to build a life that remains enjoyable and sustainable over the long run. They want to continue practicing medicine without feeling trapped by it. They want to spend meaningful time with their families. They want enough financial resilience that future decisions can be made thoughtfully rather than under pressure.

In many ways, they’re searching for the same thing I was searching for: not necessarily freedom from work neither early retirement, but just a greater degree of control over how their time, energy and attention are spent.

The older I get, the more I think that’s the real conversation. Traditional financial advice is often mathematically sound and, for many people, it’s more than sufficient. But physicians aren’t simply solving for mathematics. They’re navigating a career path with unique rewards, unique challenges and a timeline that looks very different from most other professions.

And because of that, the most important financial question often isn’t how much wealth you’re accumulating, but what that wealth ultimately allows you to do.

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions