This fall, I’m switching from normal health insurance to a high deductible plan with an HSA (health savings account). HSAs are the holy grail of personal finance because they’re triple tax advantaged. Are you excited yet? Read on.

This post may contain affiliate links.

The FIRE community is an interesting bunch. While a normal conversation between friends might include kids, football, or workplace drama, FIRE community conversation is very different.

People who pursue financial independence are more likely to talk about the subtle differences between the flavors of FIRE: lean, fat, or morbidly obese. There’s even a particular category called barista FIRE.

Barista FIRE is interesting for a couple of reasons. First of all, after college I worked as a barista in the year before I started medical school. So I’ve got a soft spot in my heart for coffee shops. But more importantly, I find it fascinating that this type of FIRE even exists as a concept.

Barista FIRE’s existence is a striking commentary on the state of healthcare in the United States. To explain, barista FIRE entails being financially independent, but working part time (generally as a Starbucks barista) solely for the purpose of getting health insurance. It’s a way to insure against catastrophic increases in the cost of healthcare, which in the US are already among the highest in the world and growing.

As a physician, I’m complicit in this dysfunctional system. But it’s not a simple problem to solve. It’s a Gordian knot of governmental agencies, insurance companies, and pharmaceutical behemoths.

As a FIRE community, we continue to figure out ways to achieve financial independence and also fund future healthcare costs. A health savings account (HSA) is a fantastic way to do this .

How to get an HSA

Before I get into why HSAs are the “holy grail” of personal finance, I should fill you in on a very important detail. You can only get an HSA if it’s paired with a high deductible health plan (HDHP). If this doesn’t apply to you, feel free to bookmark this post for the future.

Basically, HDHPs are generally cheaper than traditional health plans, but they have a higher deductible. So you’ll pay higher out of pocket expenses for medication, services, and procedures until you meet your deductible. After you do that, all extra costs will usually be covered with a copay.

The deductibles change every year, but here’s what it is for 2020:

For 2020, the IRS defines a high deductible health plan as any plan with a deductible of at least $1,400 for an individual or $2,800 for a family. A HDHP’s total yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) can’t be more than $6,900 for an individual or $13,800 for a family.

heathcare.gov

Employers like HDHPs because they’re significantly cheaper to provide for employees. The higher deductible decreases utilization of health services because most people don’t like paying full price for services instead of a small copay. Until the deductible is met, the employee is paying for all of their services out of pocket.

So why would employees be ok with a HDHP? It sounds like a bad deal. The saving grace, and the reason why I’m psyched, is the ability to use a Health Savings Account (HSA).

Why HSAs are so amazing

At its most basic level, a health savings account (HSA) is a savings account for medical expenses. What makes it special are the rules around it that together make HSAs the holy grail of personal finance.

HSAs are triple tax advantaged. In other words:

HSA rules

- Money goes in pre-tax.

- Money can be invested and it grows tax-free

- Contributions roll over from year to year.

- You withdraw it tax-free, as long as it’s spent on qualified expenses.

In comparison, a 401(k) retirement account is only double tax advantaged:

401(k) rules

- Money goes in pre-tax.

- Money can be invested and it grows tax-free.

- Contributions roll over from year to year.

- You’re taxed when you withdraw the money in retirement.

What can you spend an HSA on?

Money you save in an HSA can be spent on any eligible medical expense for you and your dependents. According to the IRS, this is any expense to “alleviate or prevent a physical or mental disability or illness.” For example:

Covered medical expenses

- Doctor visits, hospitalization, or surgery

- Prescription medication, supplies, and devices

- Acupuncture, chiropractors, optometry, and mental health services

- Insurance premiums, long term care

The list of qualified expenses is very broad, but there are exceptions. The expense can’t be for something that’s just generally beneficial to your health, like vitamins or a Caribbean vacation. There are some other things that aren’t covered.

Uncovered medical expenses

- Childcare and diapers

- Cosmetic surgery

- Funeral services

- Gym or health club fees

- Nonprescription medication

How much can you save in an HSA?

You are able to save a considerable amount of cash in HSAs, but the exact amount depends if you’re saving individually or as a family.

2020 HSA Savings limits

- Individual: $3550 per year

- Family: $7100 per year

Source: Heathcare.gov

Why am I excited about this?

I didn’t care too much about HSAs before this year, despite their holy grail status. In fact, I actively ignored their existence because I was bitter that I didn’t have access to them. But recently, we got word that my employer will be offering a high deductible health plan with a health savings account starting this fall!

I currently have great health insurance. It’s a normal plan with low copays and no deductibles. But honestly, we don’t use it very much. Thankfully, my family is fairly healthy with no chronic illnesses yet. We do very basic things every year like checkups and vaccinations.

So when I learned of the option to switch to a high deductible health plan (HDHP) and utilize an HSA, I got really psyched about the possibility of insuring against future healthcare costs.

How much money can I accumulate?

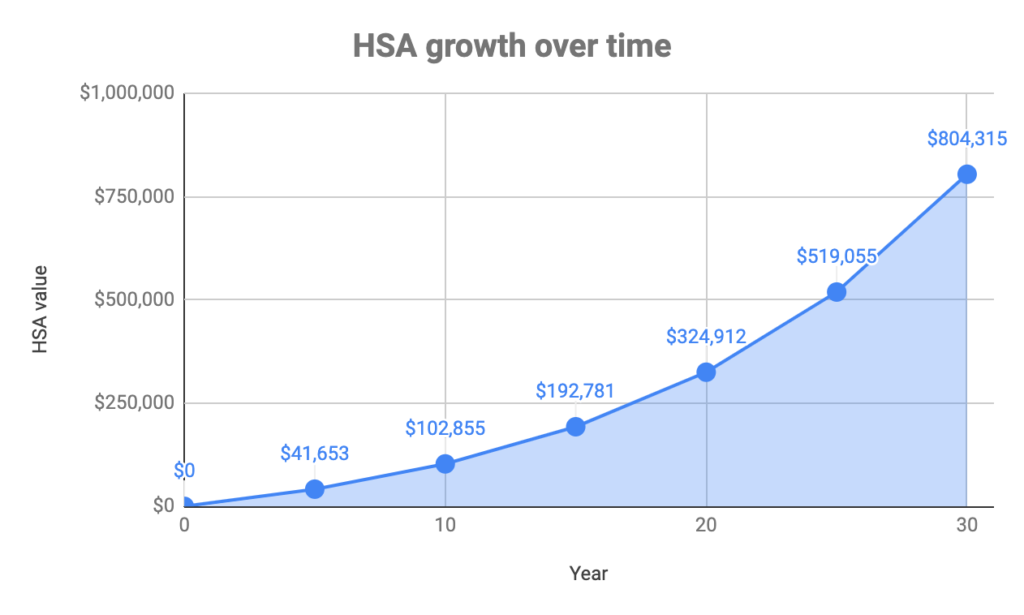

For the purpose of this calculation, let’s say I save the maximum family contribution for 2020, $7100, annually. This is going in pre-tax, so it’ll be much easier to fund this investment. Let’s also assume that I have no healthcare expenses and I can invest this money at 8% gain annually.

Here’s the growth of $7100 invested annually over 30 years:

That’s a lot of money set aside for future healthcare costs!

Downsides of an HSA

A big downside of an HSA is that it can only be offered alongside a high deductible health plan. For our HSA, this means that I’ll need to meet a $2800 deductible each year before my family healthcare costs are covered by the insurance plan in a similar way to a traditional plan.

So if you anticipate you’ll have lots of healthcare costs and you don’t think you’ll have extra money to contribute to the HSA, perhaps this isn’t a good option. But if your family is relatively healthy and you plan to take advantage of the extra saving vehicle of the HSA, a high deductible health plan could be a great fit.

The worst case scenario

Let’s say I sign up for the high deductible health plan this fall and put away the maximum allowable into the HSA: $7,100. Next year, say I get sick and spend the maximum deductible for my family: $2,800.

This is roughly the amount of money that I’ve saved on taxes by putting money into the HSA pre-tax. Taxes on $7,100 at a 40% tax rate would have been $2,840.

So as long as I fully utilize the HSA, it all comes out to a wash, even in a year of high utilization of healthcare.

HSA tips

Here’s a ninja tip for HSAs: there’s no current limitation on when you have to reimburse yourself from the account.

For example, I could pay $100 out of pocket for acupuncture tomorrow, save the receipt, and reimburse myself from the HSA in 20 years.

Why would I do this? Because it gives that $100 twenty years of tax free compounding growth in the HSA before I take out the money!

After 20 years of compounding at 8%, that $100 will have grown to $466. So by deferring that cost, I’ve made $366 of growth in the HSA.

Another tip is that you can still use HSA money for non-qualified expenditures.

In 20 years, perhaps the US will have an excellent system of socialized medicine (stop laughing please). If that happens, I’ll have little use for an HSA. But I can always just pull out the money and use it to buy a Tesla. Since this is a non-qualified expense, I’ll get taxed on this money just like if the HSA was a 401(k) and play a 20% penalty. Ouch.

But if I’m 65 years or older when I do this, there’s no additional penalty, and the HSA is treated just like any other pre-tax retirement account.

Conclusion

Health Savings Accounts (HSAs) are the holy grail of personal finance because they’re triple tax advantaged. No other account can match this. They can give you flexible options in retirement to cover your medical expenses and insure against runaway healthcare costs. At worst, it’s like having another 401(k).

The major downside is that it has to be paired with a high deductible health plan (HDHP). But if you and your family are relatively healthy, this isn’t necessarily a big problem.

I don’t think a HDHP with HSA makes much sense unless you think you’ll be able to invest in the HSA to the maximum. But if you have the cash to do that, you could definitely come out ahead in the long run.

Given the growth of my real estate empire, there’s a good chance that I’ll be financially independent much faster than most of my peers. In fact, I feel this is a virtual certainty. When I reach this goal, I’d rather be morbidly obese FIRE (moFIRE) instead of barista FIRE. An HSA can help make this a reality by giving me more options for funding my healthcare.

All in all, I’m excited to sign up for the high deductible health plan this fall so I can start saving into the HSA. Given the trend of healthcare costs in the US, I’ll be glad I set aside the money!

–TDD

Do you agree HSAs are the holy grail of personal finance? Comment below and tell me your experience with it! Please share and subscribe for more content.

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

TDD,

There is definitely a tax and growth advantage to HSAs.The FIRE community may be rare in that it is thinking about both of these benefits.

On the contrary, I have many patients with HDHPs and they often forgo care because they incur all the costs up front until their deductible is met. I’m not sure how many of them even max out their HSAs, but I don’t think they fully understand all of the advantages.

I don’t have access to one, but it sounds like you are fortunate to have the high marginal tax benefits. Looks like Christmas came early for TDD’s household!

Haha, thanks Medimentary. I agree that high deductible health plans are only a blessing when combined with maxing out the Health Savings Account. If you don’t take advantage of the HSA, you’re definitely on the short end of the stick and only your employer wins. — TDD

Totally agree with the benefits of an HSA, but California and New Jersey eat into this triple-tax advantage. One of the reasons I haven’t explored this option further is because contributions and earnings are taxed at the state level in only these two states (I’m in CA), for whatever reason. Still a useful tool, but a little bit messier out here.

California state taxation is ruthless. Absolutely ruthless.