Today I discuss an asset protection option for California real estate investors: the Delaware Statutory Trust.

This post may contain affiliate links.

Disclaimer: this is not legal advice. I’m just communicating what I’ve learned about this topic from my personal experience and research. Consult a legal professional before making any decisions.

One of the major concerns that holds back potential real estate investors is asset protection. The United States is a litigious country, and a common saying amongst real estate investors is: “It’s not a matter of if you’ll get sued, it’s when.”

Just as physicians need malpractice insurance, it’s important for real estate investors to have appropriate liability protection too. Unfortunately, I often see investors paralyzed by this step. They become so worried about creating a separate legal entity to protect them from being sued that they never get started. They’re so paralyzed by the legal aspects that the crucial first investment property never gets purchased. Years later, they will still be yearning for cash flow and financial independence, but will be no closer to that goal.

The most common option: the LLC

Asset protection for real estate investors is usually pretty straightforward.

The most common form of asset protection is the LLC (limited liability company). This is an entity that is created for the purpose of asset protection. It “owns” the company in a legal container that is walled off from the rest of the owner’s assets.

When it comes to real estate, investors use LLCs to legally contain their properties. You simply create an LLC (with or without the help of a lawyer), and legally move your property into the LLC. Now on paper, you don’t own the property anymore. The LLC does. While this seems to be just semantics, it’s legally quite powerful.

In the ideal scenario, even if a tenant sues you, the only real property that can be consumed in the lawsuit are the assets contained within the LLC. Your other assets like your primary home and personal bank accounts should be shielded from seizure.

If there are multiple properties, the most common structure currently is a series LLC. This is a structure where multiple LLCs are organized in parallel. They’re legally isolated from each other, so one LLC could be sued and should not affect the others. An umbrella LLC (or master LLC) exists on top of the series that “owns” all of the child LLCs. This puts one more onion layer of protection between the investor and the properties.

California Real Estate Investors

Real estate investors in California have it rough. California has sky-high acquisition costs, strict rent control, and laws that favor the tenant over the landlord. Furthermore, the most common form of asset protection, the LLC (limited liability company), is specifically taxed in California. In fact, the California Franchise Tax Board levies an $800 tax (as of 2021) for each LLC that is “doing business or organized in California.”

Californians get ample sunshine, culture, and diversity. But the state really makes you pay for these luxuries. The franchise tax is just another example of the “sunshine tax.”

This tax can quickly add up when you have multiple properties. Therefore, individual investors have a tough choice. Do they just use insurance alone for liability protection, or do they put everything into LLCs and significantly increase their legal costs?

This LLC tax is not a trivial dollar amount. There are many deals where the extra cost of $800 annually can really eat into the profit margins.

I feel that this LLC tax is a significant disincentive for business formation in California, but I suppose that’s besides the point. The law exists.

Do you really need to pay the Franchise tax?

This is a question that is asked when investors first find out about the franchise tax. Is this for real? Do I really have to pay this?

To start this discussion, I’d emphasize this only applies to California based investors. If you live somewhere other than the Golden State, you don’t need to worry about this. Create LLCs to your heart’s content.

But it’s a good question. Let’s look at the two options when it comes to LLC formation for California real estate investors:

- Form LLCs and pay the franchise tax for each one

- Form LLCs in other states and don’t pay the tax

The most conservative option is #1. You’ll never get in trouble for paying all the potential tax owed. If you form the LLCs in California, the tax board will notice these and bill you. Just accept the franchise tax as a cost of doing business and move on.

But LLCs don’t need to be formed in the state where you live. So you can choose option #2: form your LLCs in other states and plan to not pay the Franchise Tax. This option has the risk that the California tax board may (at some point) notice that you own these LLCs, and bill you for both the unpaid franchise tax and penalties.

I should note that I know of one prominent law firm that recommends ignoring the Franchise Tax altogether. They do not feel the tax is lawful, and state that they’ll defend you against attempts by the Franchise Tax Board to collect on the tax. But to be honest, I know of no specific instance where this took place. For many of my investor friends, this option is therefore too nerve-wracking.

Thankfully, there is another option: The Delaware Statutory Trust.

The Delaware Statutory Trust

After the passage of the Delaware Statutory Trust Act in 1988, the state of Delaware became the first state to adopt a set of laws around trusts. Investopedia defines a trust as “a fiduciary relationship in which one party, known as a trustor, gives another party, the trustee, the right to hold title to property or assets for the benefit of a third party, the beneficiary.”

The Delaware Statutory Trust was enshrined in Delaware law as the first set of laws specifically for utilizing a trust for asset protection.

I’ll refer to this entity from now on as a DST. It is one of the most versatile legal entities I’ve ever seen.

Like a normal trust, the DST can have trustees as well as a group of beneficial owners. The trustee(s) can be the same as the beneficial owner as well.

The DST model has gained favor with California real estate investors because it has all the legal power of an LLC, but is not an LLC.

How the DST is used in real estate investment

If you Google “Delaware Statutory Trust,” you’ll most likely come across information about using a DST to form the investment vehicle of a 1031 exchange. ( A 1031 exchange is a form of tax deferral after the sale of a real estate asset.)

This model allows any number of investors to defer capital gains via fractional interest in the DST. If this doesn’t make sense, don’t worry. This isn’t how you use a DST for asset protection.

Delaware Statutory Trust for Asset Protection

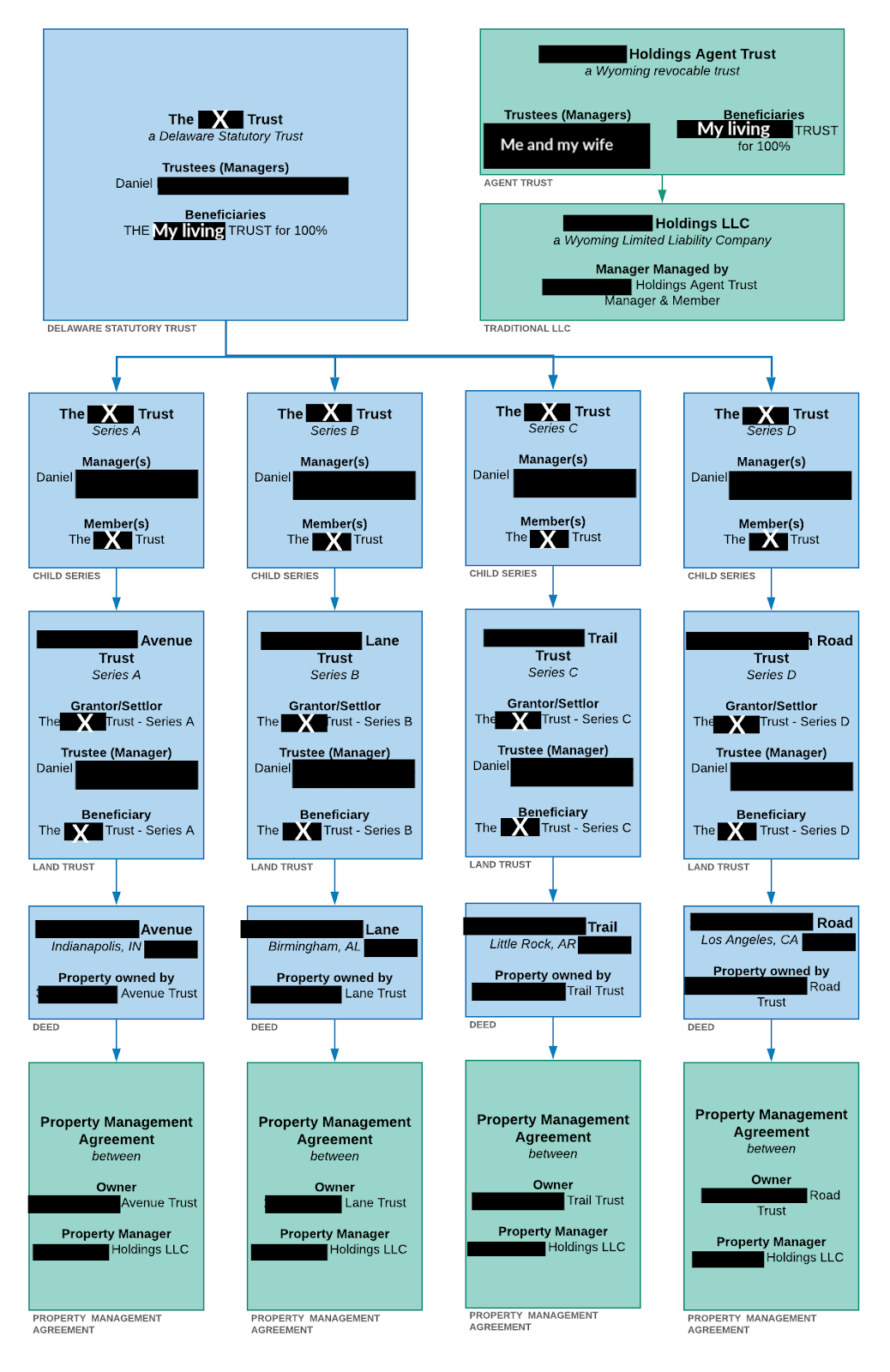

To break it down in simple terms, a DST can act almost exactly the same as a series LLC model, without requiring the formation of multiple LLCs.

After formation, the DST becomes an entity that is like the master LLC in the series LLC model. It’s the outer shell of the real estate investor’s property holdings. Acquired properties are then placed into “child series” within the DST via legal containers called land trusts.

All of these layers put up legal barriers between the beneficial owners and the underlying asset. This limits the personal liability of the owners in the same way as LLCs.

This also has the added benefit of less stringent reporting and paperwork requirements.

How Delaware Statutory Trusts benefit California investors

The Delaware Statutory Trust structure for asset protection has a number of benefits for California investors:

- No LLCs (and no franchise tax requirements)

- Anonymity (the owner’s name doesn’t appear on the deed anymore)

- Less liability: legal fallout from one property is siloed from the other properties

Here is an anonymized schematic of how this actually works from my own portfolio from about a year ago. You’ll note that the beneficiary of the DST is my living trust. This is one more onion layer of protection my family has, and it greatly simplifies our estate planning. I’ll write about it in the future.

Here is our schematic:

Wait, there’s still an LLC!

Yes eagle eyes, there is still one real LLC (upper right hand corner). When I formed my DST structure, it was recommended to have one “operating LLC.” This LLC will essentially be a conduit for all of the flows of cash, while owning no actual personal property.

The operating LLC is the public facing part of your entity structure. As its own legal entity, the operating LLC can do business on behalf of the DST.

My operating LLC is responsible for holding rental income and disbursing funds to repair, renovate, and maintain my properties. It’s the company that I put down on contracts with property management and utility companies. But it’s just a conduit for money. It owns no other assets other than what’s in its business checking account.

The DST is simply the legal container that is responsible for holding my physical properties.

The articles of organization (created by my law firm) give my operating LLC the power to do business on behalf of the DST and the land trusts which technically own the properties.

How this affects my taxes

Both the DST and my operating LLC have tax IDs (EINs). But they’re disregarded entities and the income passes through them to my own taxes. For federal tax purposes, I report the income and expenses of my real estate business on my personal tax return.

But having formal tax IDs for the DST and operating LLC is still helpful. It allows for business checking accounts that help keep my accounting books nice and clean. This helps me keep track of capital contributions to the business, as well as income and expenses.

These balance sheet advantages help immensely when it comes time to do my taxes.

How well does the DST model stand up to legal challenges?

There is a concept in LLCs called “piercing the corporate veil.” It basically means that if the liability is so egregious or the legal documentation isn’t ironclad, a judge can break through LLC protection and go after personal assets. I mention this to say that no asset protection is foolproof.

My law firm contends that the DST model has stood up to legal challenge, but it’ll never have as much case law behind it as the LLC model. At the end of the day, we have to give some trust to our advisors in this matter. Thousands of investors have chosen the DST model for their asset protection.

How you set up a DST for Asset Protection?

I set up my own DST structure through Royal Legal Solutions. This is a boutique law firm in Texas that specializes in asset protection for real estate investors. They have a particular niche when it comes to the use of the Delaware Statutory Trust for California investors.

I’ve been a customer of Royal Legal since 2020 and overall I’ve been very pleased. I wouldn’t say they’re the cheapest option, but they give a good concierge experience. I’ve found them responsive to my inquiries and quite professional in their communication. And more importantly, I feel reassured that I’m reducing my liability from my real estate business.

You can contact them below to book a paid consultation! (*Affiliate form*)

Contact form for Royal Legal Solutions

Conclusion

At the end of the day, insurance and asset protection will help you sleep at night. They’re important to mitigate risk. But in my mind, the true purpose of asset protection is to free investors to take the risks necessary to invest and create businesses.

California has put up barriers to business creation because of the Franchise Tax on LLCs. But via the Delaware Statutory Trust structure for asset protection, California real estate investors have an alternative option that accomplishes the same thing as the traditional series LLC structure.

Your mind is probably spinning. It’ll help to read this over a couple of times and book a consultation above. I hope this will help break that analysis paralysis so you can move on and build your real estate empire. Let’s build our financially free futures together!

–TDD

Confused? Relieved? Comment below and please subscribe to the free newsletter below to accelerate your journey to financial freedom!

Perhaps you’re more of a Facebook type?

Are you a physician, spouse, or professional and you’re interested in using Real Estate to gain financial freedom? Join us in our Facebook group and accelerate your journey!

Want to support the blog?

- Join our investor club at Cereus Real Estate

- Visit my Recommendations page

- Check out my wife’s food blog: Eat Dessert First

- Check out my TikTok channel

- Follow me on Instagram

- Follow me on YouTube

- Contact me with questions

Thank you so much for writing this blog! I live in CA and am just beginning on my REI journey. I have been very confused by the different ways to protect assets especially for Californians. A RE attorney just recommended to me the statutory trust as a parent entity that owns the property LLCs (which in my case are not in CA for now). I’ll re-read this for sure and reach out to Royal Legal Solutions.

Thanks for commenting! I’m glad it was useful. The options are very confusing, and I hope this explained it a bit.

Hi, I’ve been told the DST is a good option and was going to go for it, but on bigger pockets rookie episode 105/106 they said it is not great for asset protection because it doesn’t matter where you form the entity, esp if you live in and your property are both outside of Delaware, Wyoming for Wyoming LLC, etc. They rec a Cook Island trust when your portfolio is big enough and a bridge trust until that point. Do you have any take on this? I’ve been trying to do my due diligence on it but am now feeling analysis paralysis. Would appreciate any insight! Thanks

Hey Laura, I think it’s a good thing to discuss with the law firm. There’s varying opinions on the location of the operating LLC vs the California Franchise tax wording. I don’t recall the conversation about the Cook Island Trust, and honestly have never heard of anyone using this at our level. That being said, asset protection is a favorite form of analysis paralysis, so I’d just pick one and move on with building your empire! In a few years, the cost of the asset protection won’t mean as much in the context of your growing portfolio!

Hi, I currently live in California, my question is, say I purchase a property in California as rental property and add that in the DST, and create an LLC from Delaware to conduct business on the property like executing rental agreements etc., do I still have to create an LLC from California or just an LLC from Delaware would suffice? Please advise.

According to my knowledge, your LLC can be located anywhere and still do business in California. But – when it comes to legal stuff, always consult a lawyer!

Hi – thanks for this… so are you paying the FTB $800 LLC tax on your operating LLC then?

I actually live in Tennessee now, so this isn’t an issue for me now. But technically yes I believe if you’re a California resident you should pay the FTB LLC fee for the operating LLC.